[[{“value”:”

[[{“value”:”

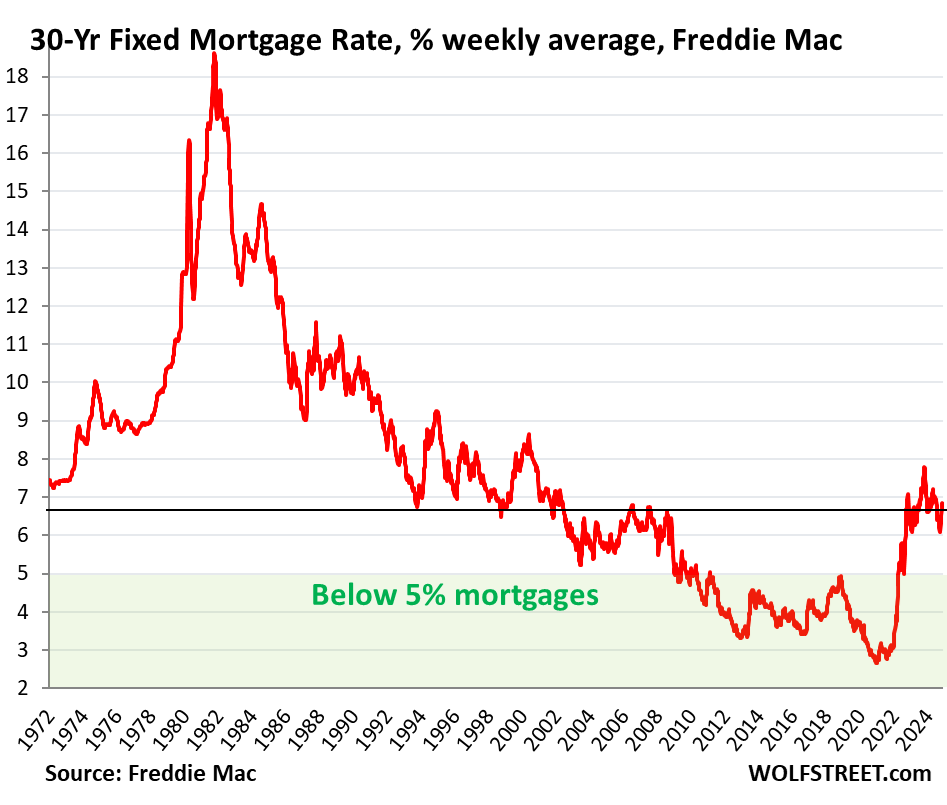

“Current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades.”

By Wolf Richter for WOLF STREET.

“It’s important for mortgage investors, the housing market, and consumers to understand that it is unlikely we will again see the low mortgage rates we had during the COVID-19 pandemic, when a unique combination of monetary and fiscal policy sent rates to near all-time lows,” wrote Priscilla Almodovar, the CEO of Fannie Mae, the largest of the Government Sponsored Enterprises that have been in conservatorship of the federal government since the mortgage crisis. They buy mortgages from lenders, guarantee them, package them into MBS, and sell the MBS to investors around the globe.

“In fact, current mortgage rates and Fannie Mae’s forecast for 2025 rates are well in line with rates over the past several decades. Since 1990, the 30-year fixed-rate mortgage has averaged 6%,” she said in the post published by MarketWatch today.

In fact, the average 30-year fixed mortgage rates were never below 5% in the data from Freddie Mac, which goes back to 1971, until the Fed started buying MBS in January 2009, which pushed mortgage rates below 5% for the first time ever.

In fact, in fact, in fact… mortgage rates were above 6% the entire time in the data until October 2002, after the Fed had embarked on slashing rates to create Housing Bubble 1 to make up for the imploded stock market. And three years later, by October 2005, after the Fed had embarked on blowing up its Housing Bubble 1, mortgage rates were back above 6% and stayed there until January 2008, when the Fed kicked off QE by buying Treasury securities to deal with the financial system that was on the brink of imploding due to the imploding mortgages. And mortgage rates began to descend, and in January 2009, with Housing Bubble 1 having collapsed and morphed into the mortgage crisis and the broader Financial Crisis, the Fed started buying MBS which pushed down mortgage rates further.

In late 2018, in response to the timid rate-hike cycle and QT, mortgage rates briefly rose to 5%. But with stocks tanking, and with Trump keelhauling Powell on a daily basis over the puny policy rates and QT, the Fed pivoted to rate cuts in 2019 and QT ended in mid-2019.

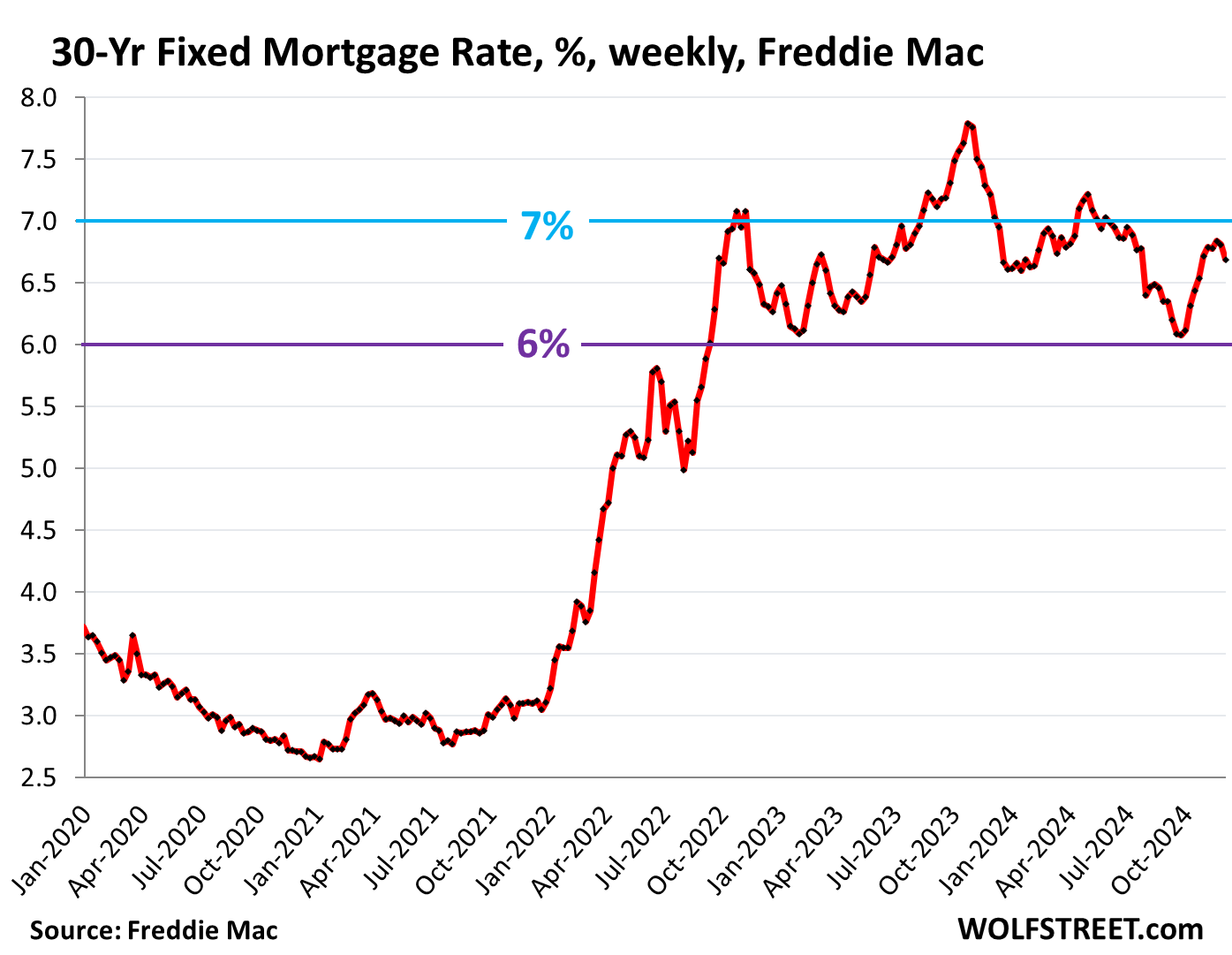

Then during the pandemic, as part of its immensely reckless QE, the Fed bought huge amounts of MBS which pushed mortgage rates below 3% for much of the time from July 2020 through September 2021, which caused the biggest inflation of home prices in the history of the data, and those inflated home prices are now the biggest problem in the housing market because it’s choking on those too-high prices and sales of existing homes have plunged to the lowest since 1995 because prices are too high.

But since September 2022, the Fed stopped buying MBS and as part of ongoing QT has shed the first $500 billion of them, and has said multiple times in its communications that it plans to get rid of them all. And mortgage rates have shot up.

In the latest reporting week, the average 30-year fixed mortgage rate dipped to 6.69%, according to Freddie Mac today. They have been above 6% since September 2022.

“Consequently, recent [mortgage] rate increases might be better viewed as simply a return to historical norms after a relatively brief period of abnormal lows, spurred by a once-in-several-generations pandemic,” the Fannie Mae CEO wrote. And then she said, essentially: everyone needs to get used to those mortgage rates.

Then she went on to explain why mortgage rates are higher, and why they’re likely to stay higher, hitting all the points we’ve been talking about here for the past couple of years.

Mortgage rates are primarily influenced by the 10-year Treasury yield, but are higher than the 10-year Treasury yield because investors in mortgages, even in government-guaranteed mortgages and MBS, face additional risks and costs over Treasuries, including the risk of prepayment. When mortgage rates drop, and borrowers either refinance the mortgage or sell the home, that mortgage with the higher rate gets paid off, and investors are paid prematurely the remaining face value of the mortgage, and that juicy income stream from the higher rates ends, and any replacements will be lower-yielding.

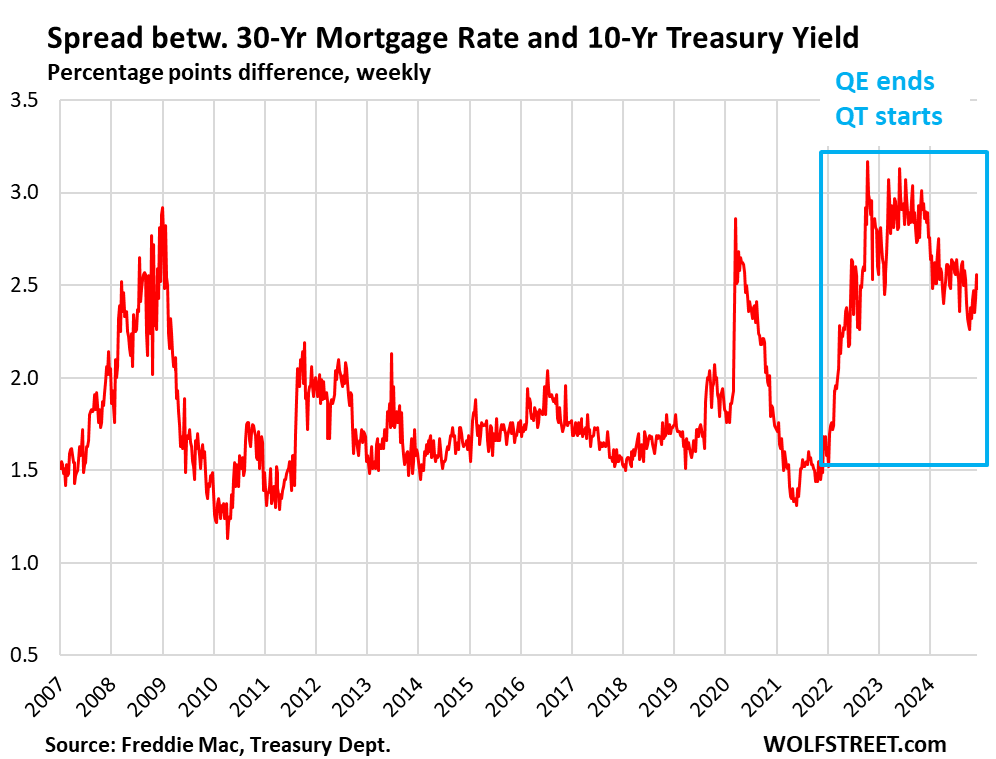

That difference between the 10-year Treasury yield and mortgage rates – the “spread” – varies based on a variety of factors.

And that’s also where the Fed’s QE and QT comes in. When the Fed engaged in QE by buying Treasury securities and MBS, it pushed down the Treasury yields and the yield of MBS, and therefore mortgage rates. In addition, the spread narrowed, and mortgage rates dropped further.

Since the second half of 2022, the Fed has been engaged in QT, shedding Treasury securities and MBS. Its balance sheet has dropped by nearly $2 trillion so far to $6.9 trillion, including the $500 billion of MBS QT. And the spread has widened over the period.

Today, the spread is at 2.48 percentage points, which is relatively wide. It went over 2% during the prior episode of QT. It then exploded in March 2020 as the market froze, but then was squashed by mega-QE. In 2022, with the announcement of QT coming, it began to widen again (blue box):

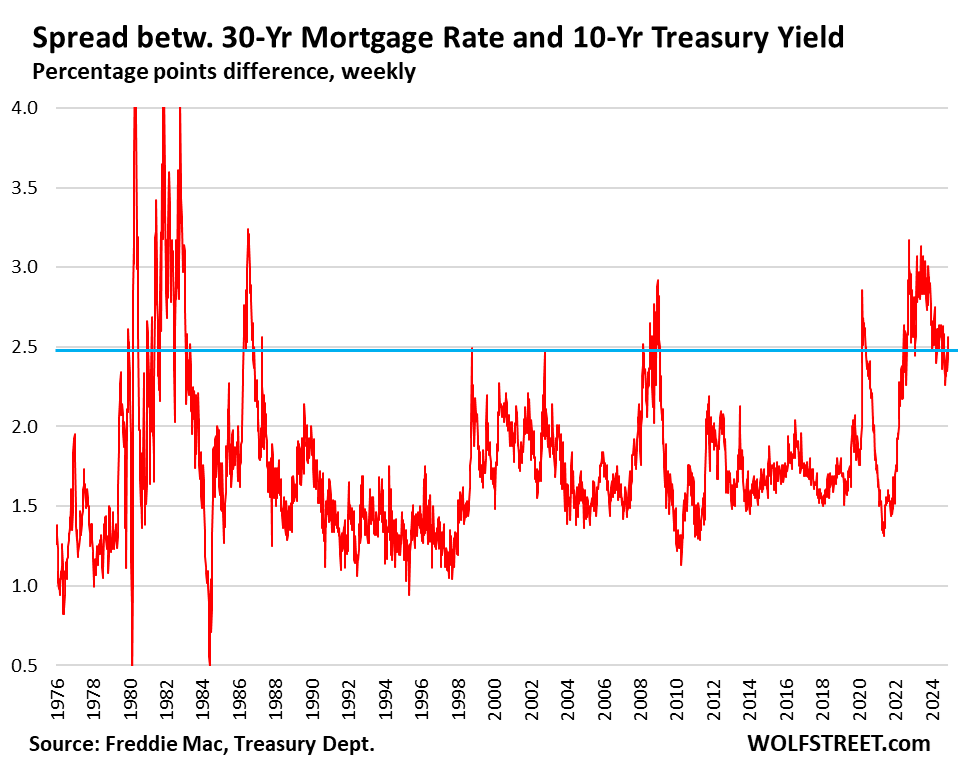

Here is the long view of the spread, which can gyrate widely when mortgage rates and Treasury yields diverge.

The spread could remain around the 2.5-percentage-point range because the Fed no longer supports the mortgage market, as it had done during QE, but instead is doing the opposite, letting its holdings of MBS run off at the pace of the passthrough principal payments. And the Fed said repeatedly that it would let the MBS run entirely off its balance sheet even after QT ends, and replace them with Treasury securities, likely with T-bills, which would take years and help keep the spread wider, all of which would put upward pressure on mortgage rates.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post Everybody Should Get Used to these Mortgage Rates, Says Fannie Mae CEO: Mortgage Rates, 10-Year Treasury Yields, QT, and Spreads appeared first on Energy News Beat.

“}]]