[[{“value”:”

[[{“value”:”

By Wolf Richter for WOLF STREET.

Yesterday, we looked at the surge of new completed “spec” houses for sale, and at the surge of new houses for sale at all stages of construction, for the US overall. Now we’ll look at at new houses for sale in the four regions of the US.

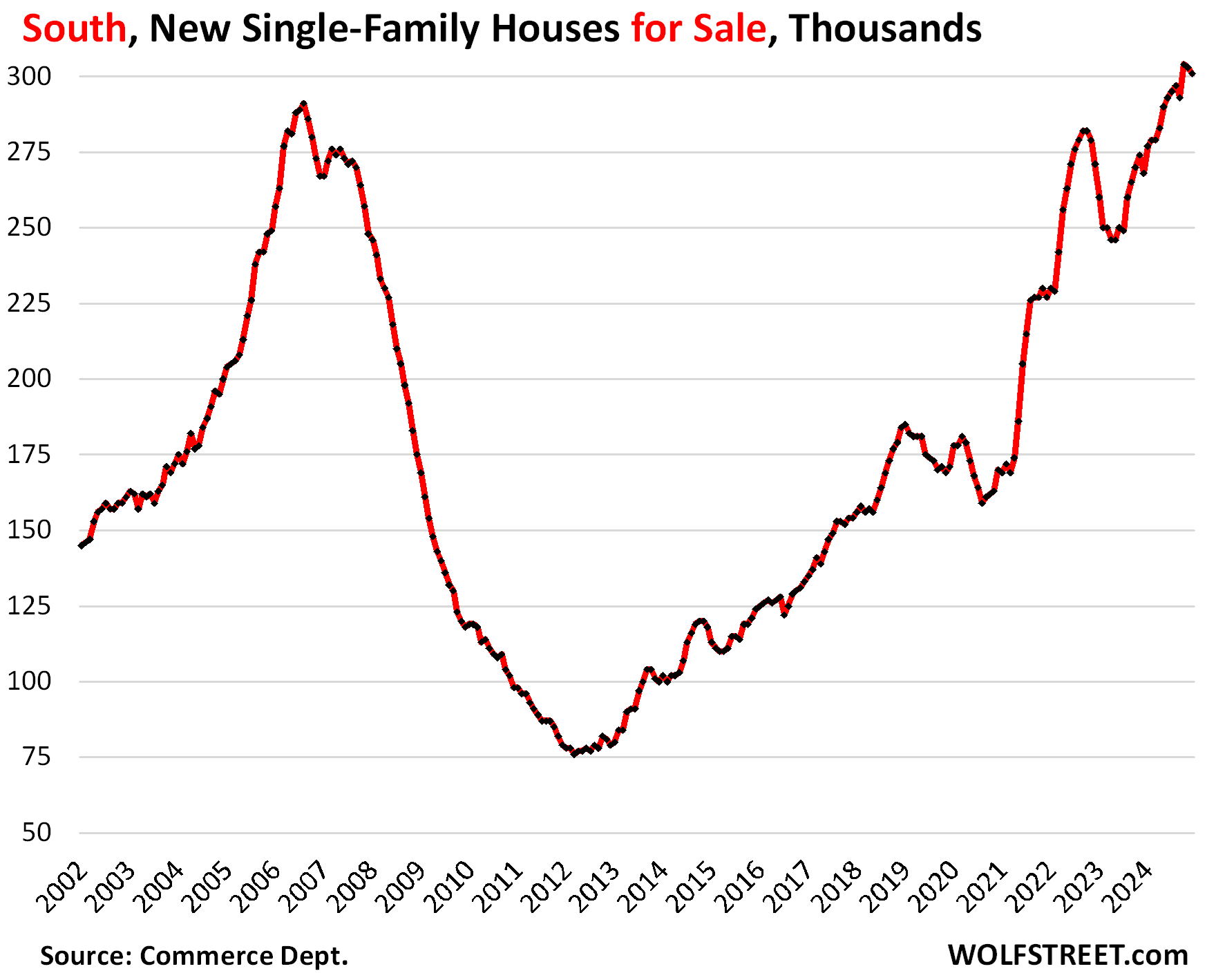

In the South – the largest region, with a population of 133 million, see map below – has the most inventory of new houses ever, surpassing even the astronomical levels on the eve of the Housing Bust, just before it all fell apart.

Since June 2024, new houses for sale in the South have surpassed the high of August 2006. In June, there were 293,000 new houses for sale (compared to 291,000 in August 2006). Since then, the inventory of new houses for sale has further ballooned and in October reached 304,000, and has remained in that range through December (301,000). Since December 2019, inventory has exploded by 76%. This is a massive amount of inventory of new houses for sale.

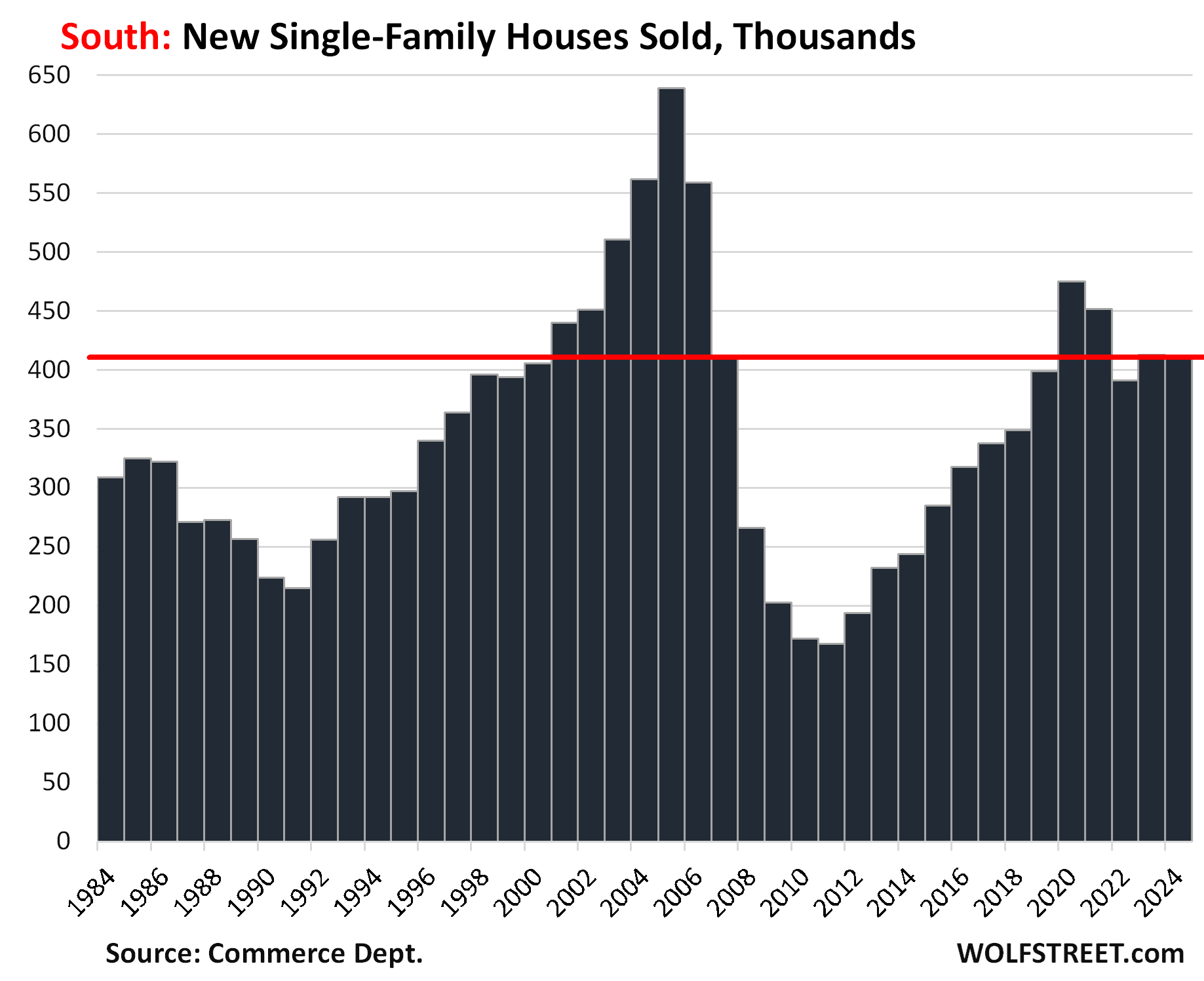

But sales of new houses in the South in 2024 edged down a hair from the prior year, to 411,000 houses sold, and was down by 13% from 2020 and by 9% from 2021, but was up by 3% from 2019.

Those sales were reasonably decent, thanks to the large-scale incentives, including mortgage-rate buydowns that homebuilders have been using to stimulate demand.

So it’s not that sales have collapsed like sales of existing homes – they haven’t – but that sales lagged far behind the speed with which homebuilders put inventory on the market over the past several years, and now there’s this glut of houses for sale.

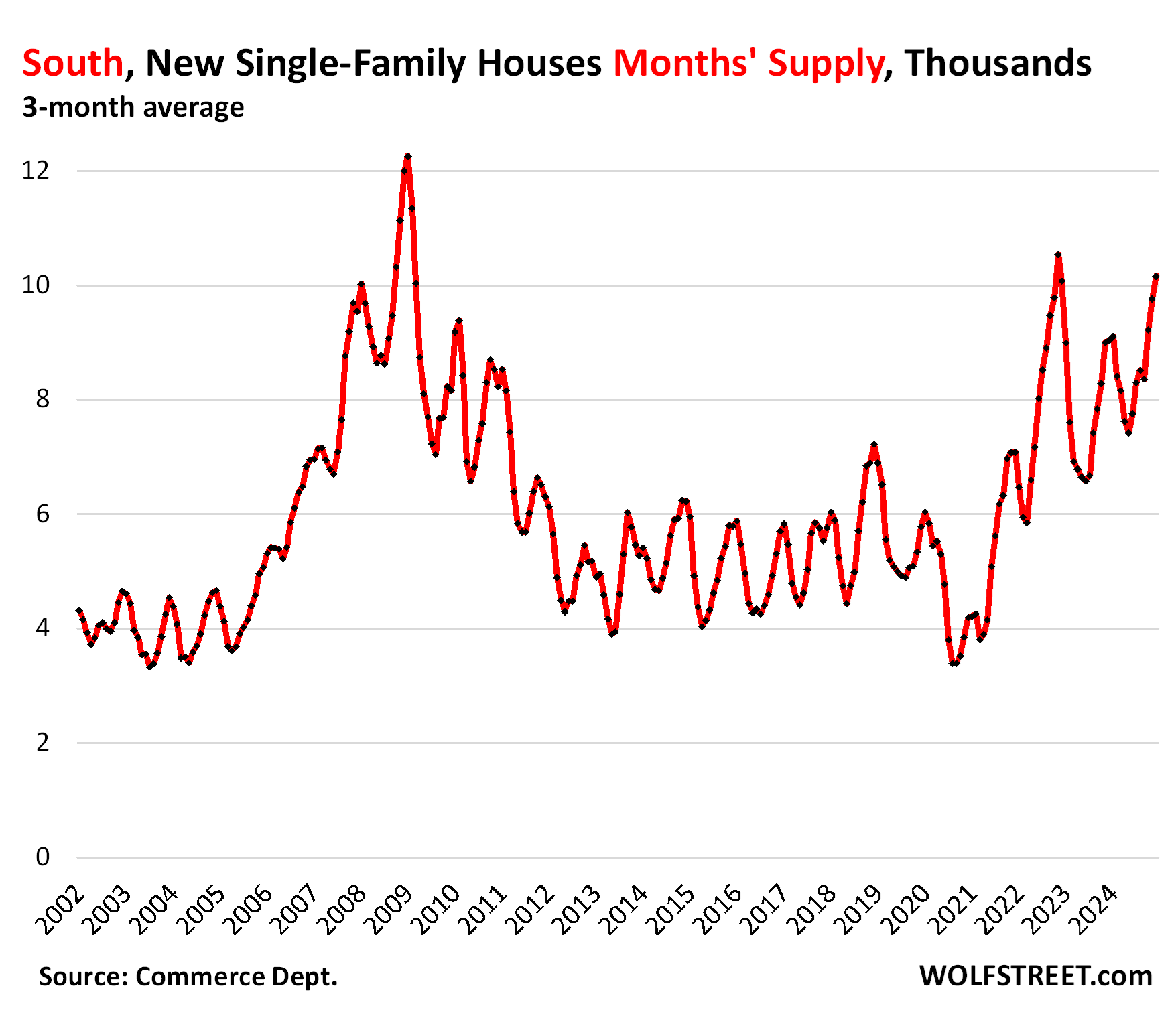

So supply of new houses for sale, at the current rate of sales, has pierced the 10-month range. To iron out some of the big monthly squiggles, we look at the three-month average. Seasonally, the peak supply period is in November through January in this three-month average. Beyond seasonality, the trend is clear, with supply having about doubled from the pre-pandemic range:

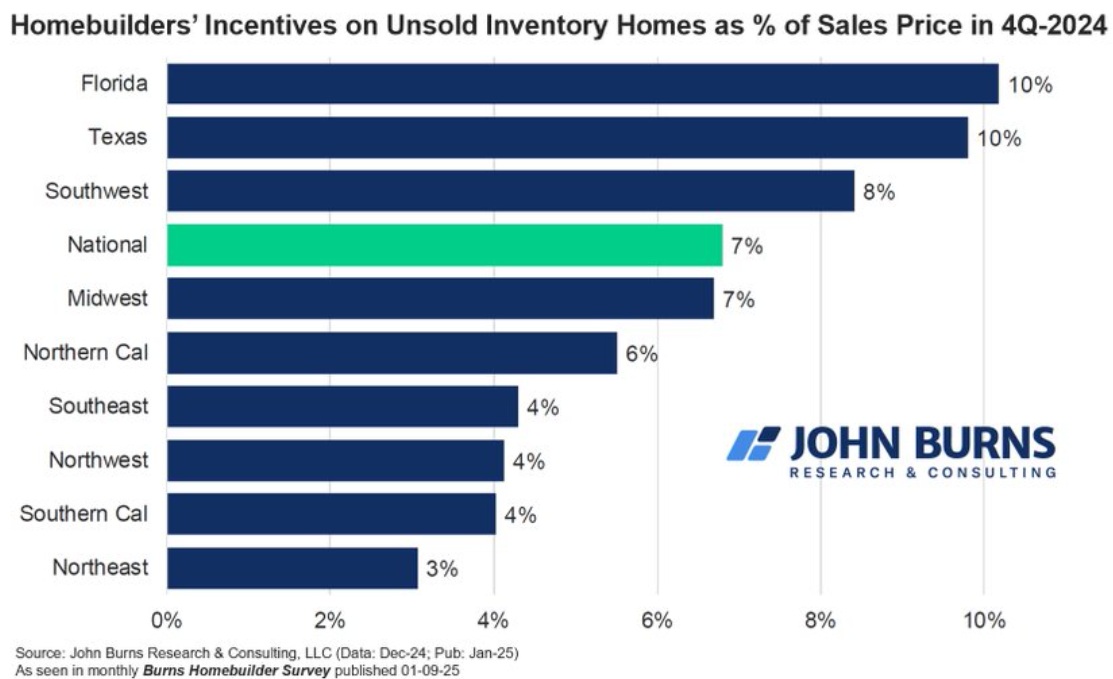

Homebuilders offered incentives amounting to 10% of the sales price on average in Texas and Florida to get the inventory moving, according to the most recent Burns Homebuilder Survey. And that’s clearly not enough to get the inventory moving.

Here is a map of the four Census regions:

The West.

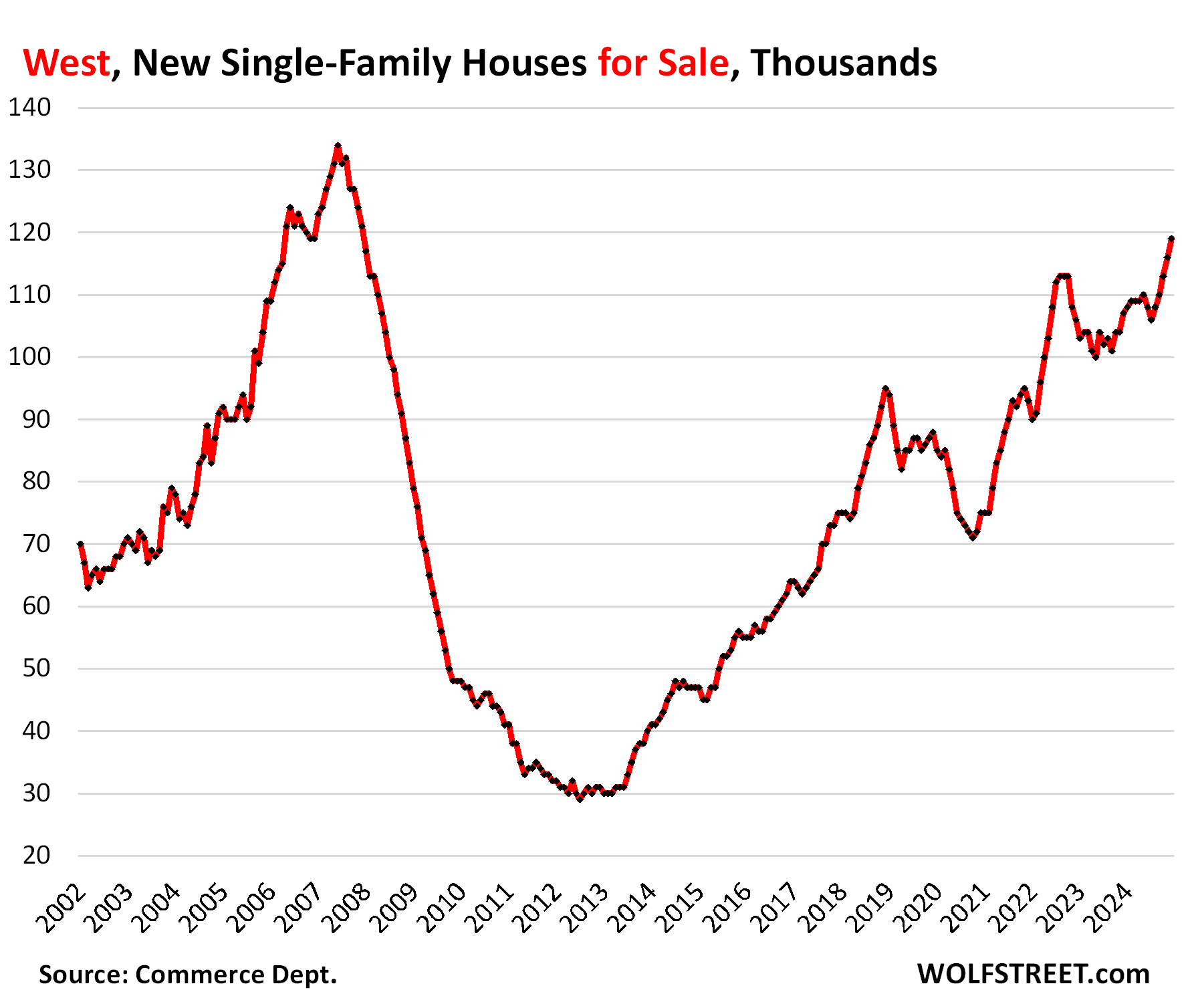

In the West – the second largest Census region, with a population of 80 million – a similar problem is piling up. Inventory of new houses for sale surged to 119,000, the highest inventory since December 2007, not far below the peak in June 2007 early on in the Housing Bust, and up by 35% from 2019:

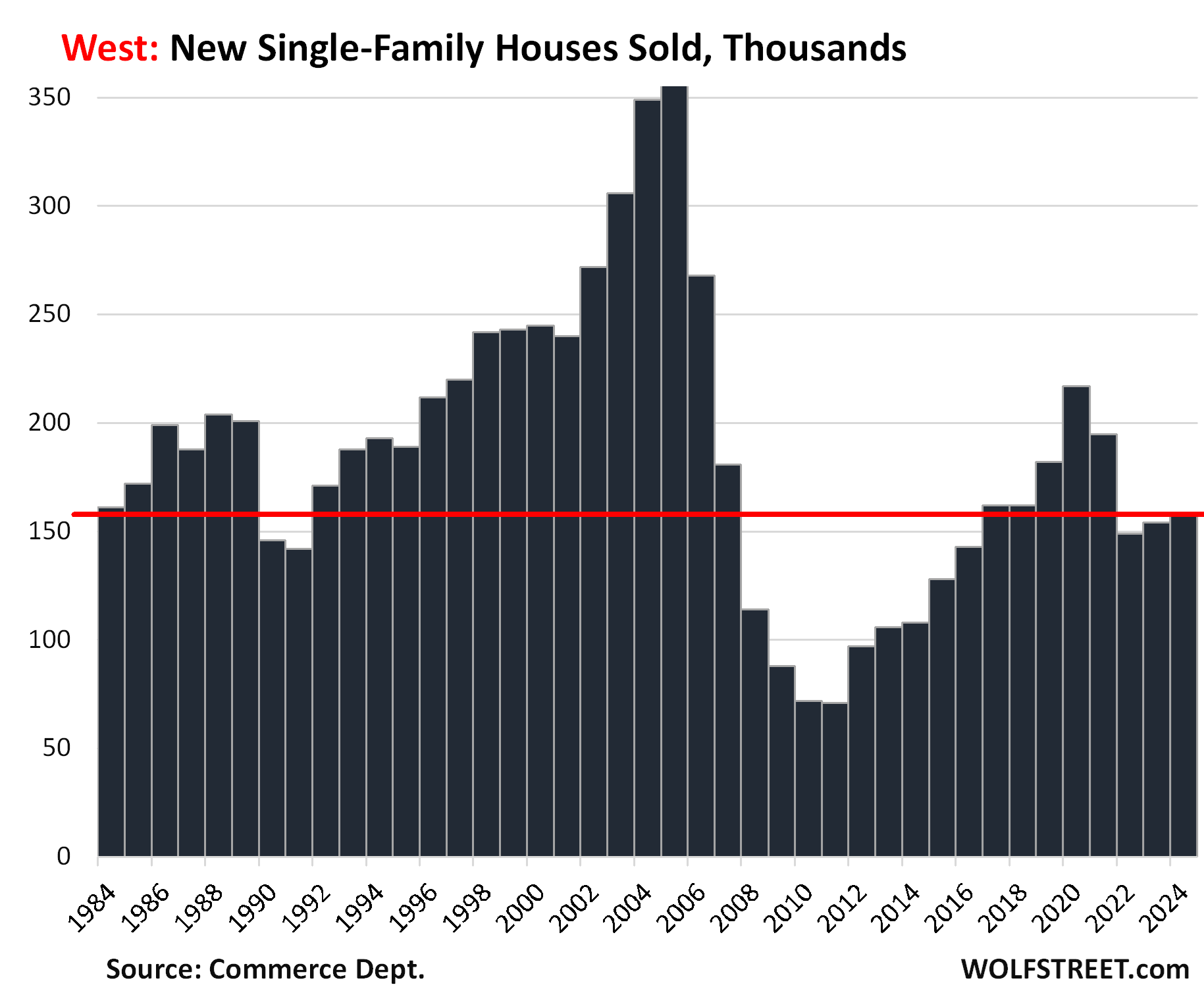

But sales have been anemic in the West because prices are way too high. In 2024, a total of 157,000 new houses were sold, down by 28% from 2020, and down by 14% from 2019. While annual sales were up from the prior two years, all three years were at the lower end of the scale, with only 2008-2016 and 1990 and 1991 having been even lower.

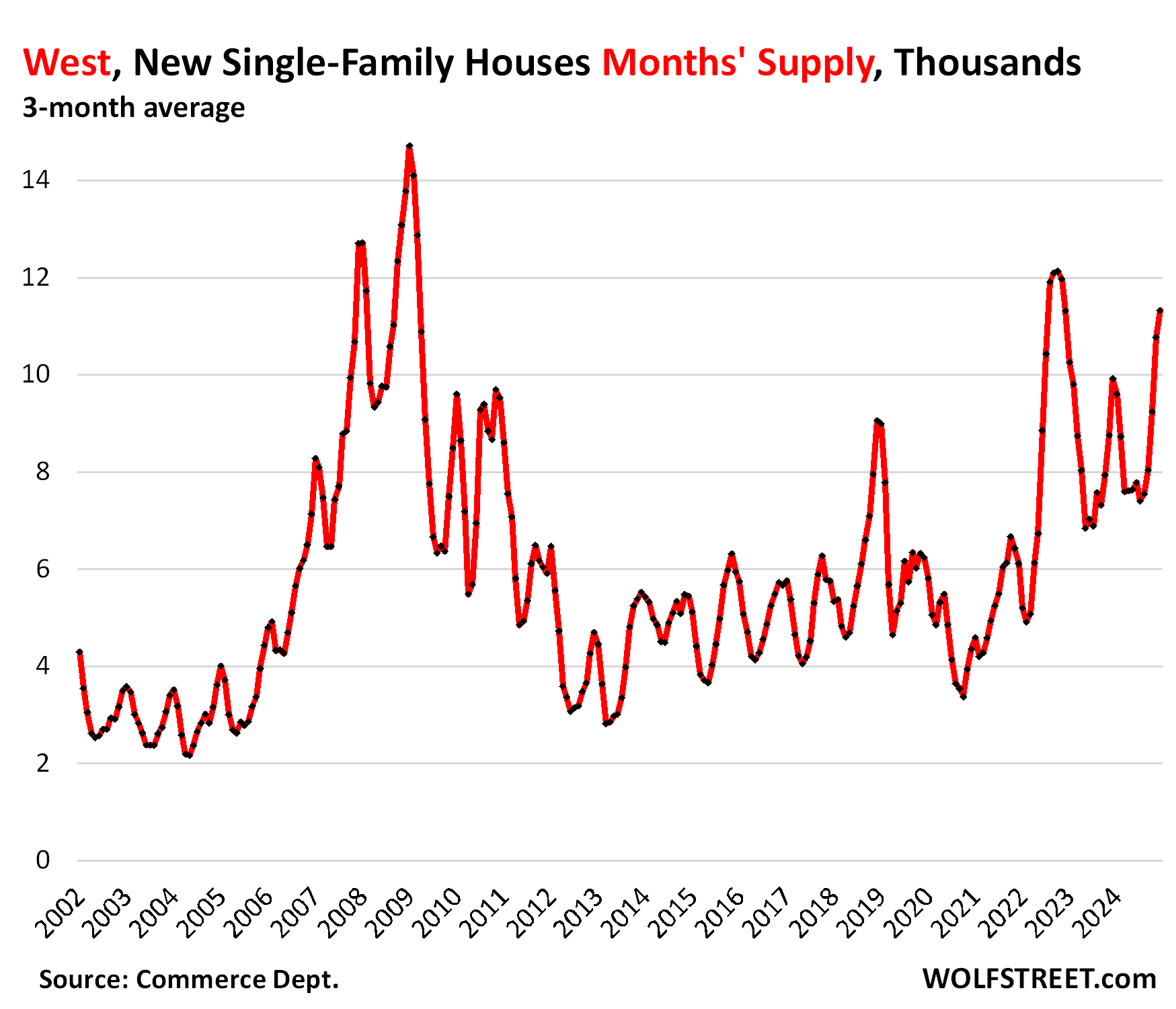

So lots of inventory piling up and sluggish sales:

Supply has therefore spiked to 11.3 months on a three-month-average basis. There were only three brief periods with higher supply:

- In late 2022 as the market for new houses was waylaid by the surge in mortgage rates, triggering a tsunami of cancellations of new-house purchases, as buyers who’s sighed the contract when rates were 3% or 4% couldn’t take delivery when rates were 6%.

- Four months of November 2008 to February 2009.

- Two months of December 2007 and January 2008.

The other two regions are not big players in the single-family market

The Northeast and Midwest are smaller in terms of the population, and much much smaller in terms of the market for new single-family houses. The regions are dominated by huge old cities, particularly the Northeast with New York City, Boston, Philadelphia, and the cities and urban areas around them. New construction is focused on multifamily to increase density and shorten commutes from the already unwieldy urban sprawl.

So there are only a few sales of new houses in those two regions, amid rising inventory and supply. But all of it is too small to really weigh on the national scale.

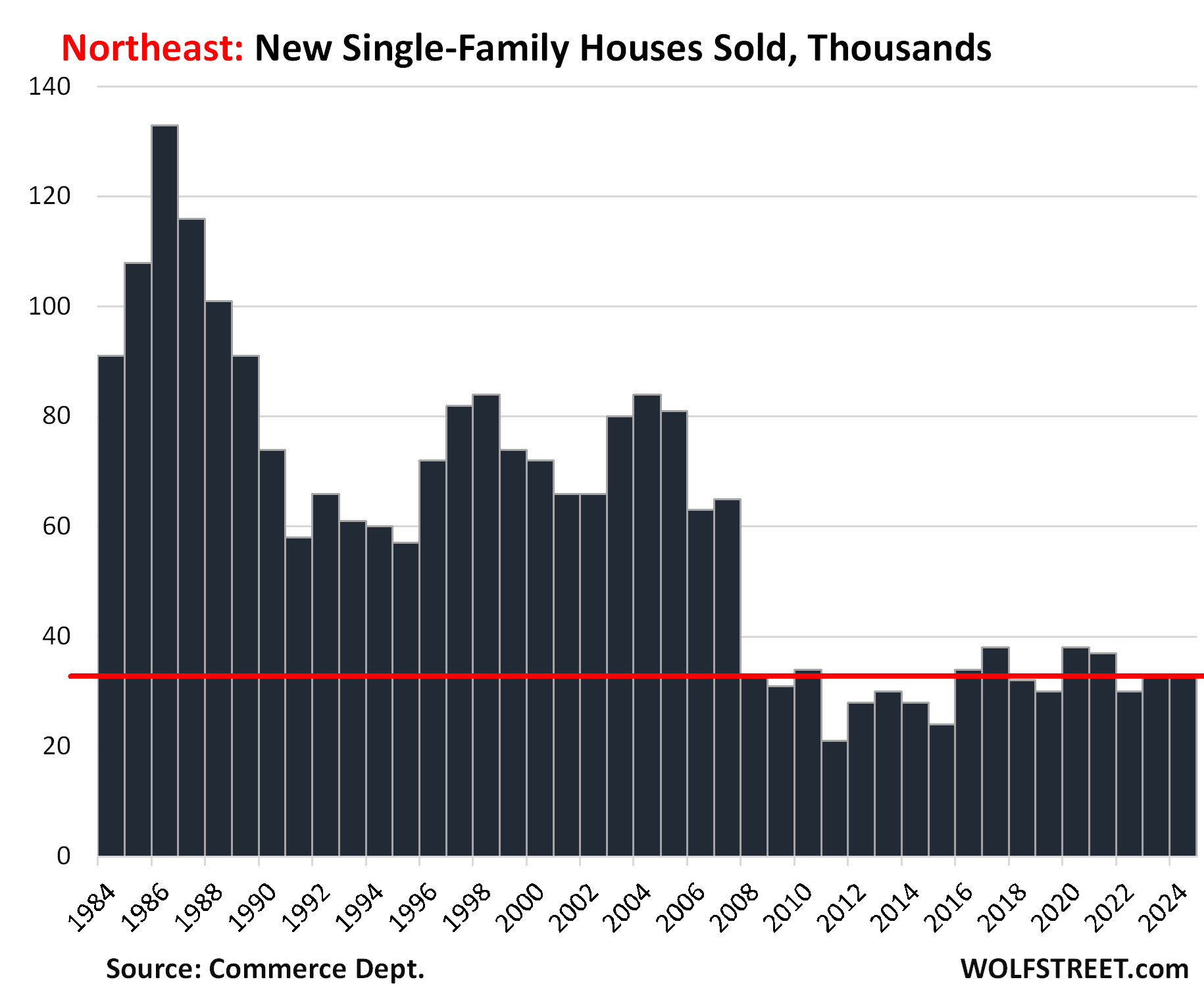

In the Northeast, only 33,000 new houses were sold in all of 2024, down by about two-thirds since the 1980s, but roughly in the range of the past 10 years.

The Census Bureau rounds sales on a monthly basis to the nearest 1,000 houses. In the Northeast, these rounded sales have been either 2,000 a month or 3,000 a month rounded. And on a few occasions 4,000 a month. We use annual sales here which would largely average out the big rounding errors of the monthly data.

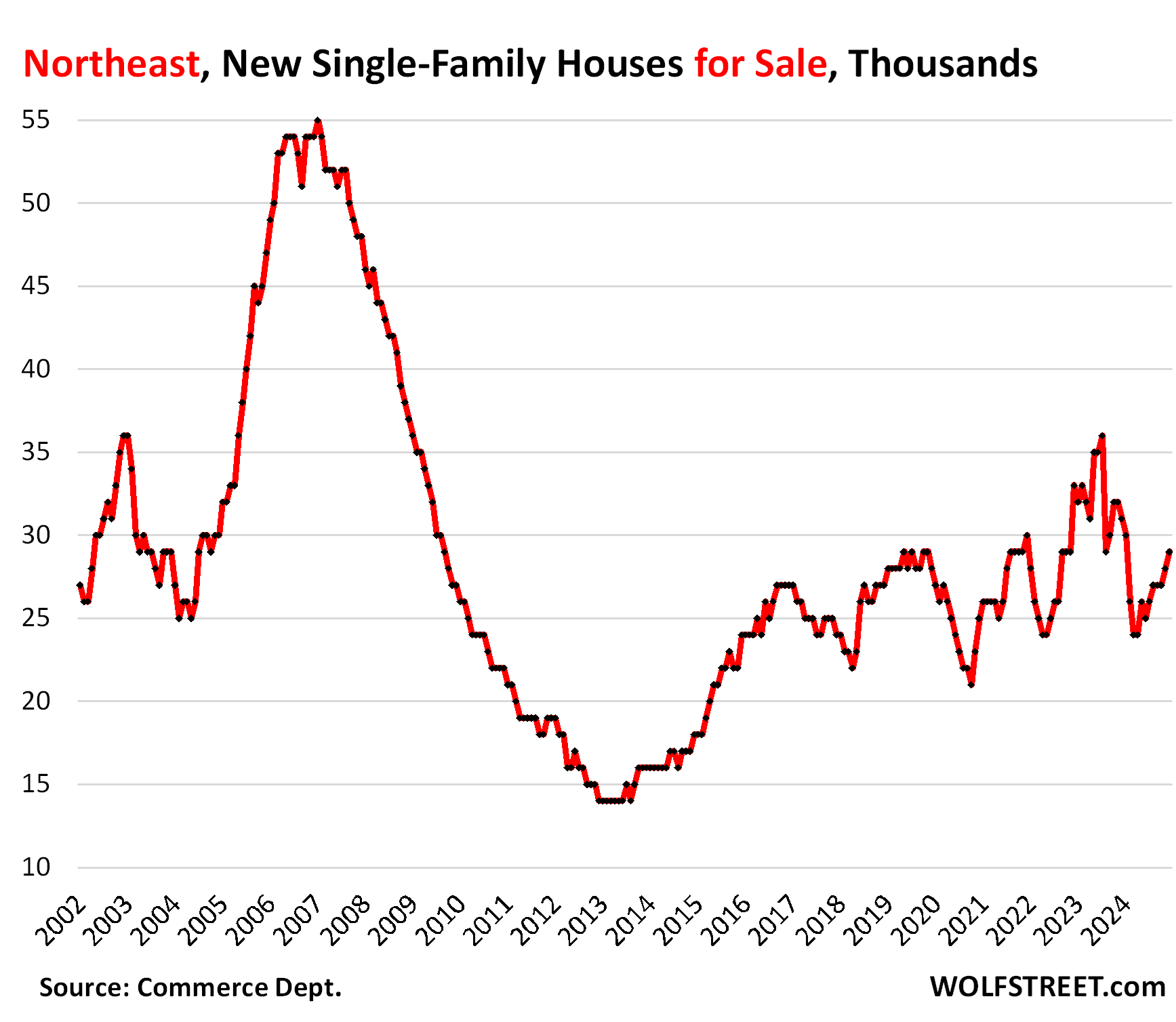

Inventory in the Northeast has been zigzagging higher over the past few years. Supply reached 17 months, by far the highest of any region. During the worst moments during the Housing Bust, supply reached 18 months. This is just not a big market for new single-family houses that would expand the urban sprawl further.

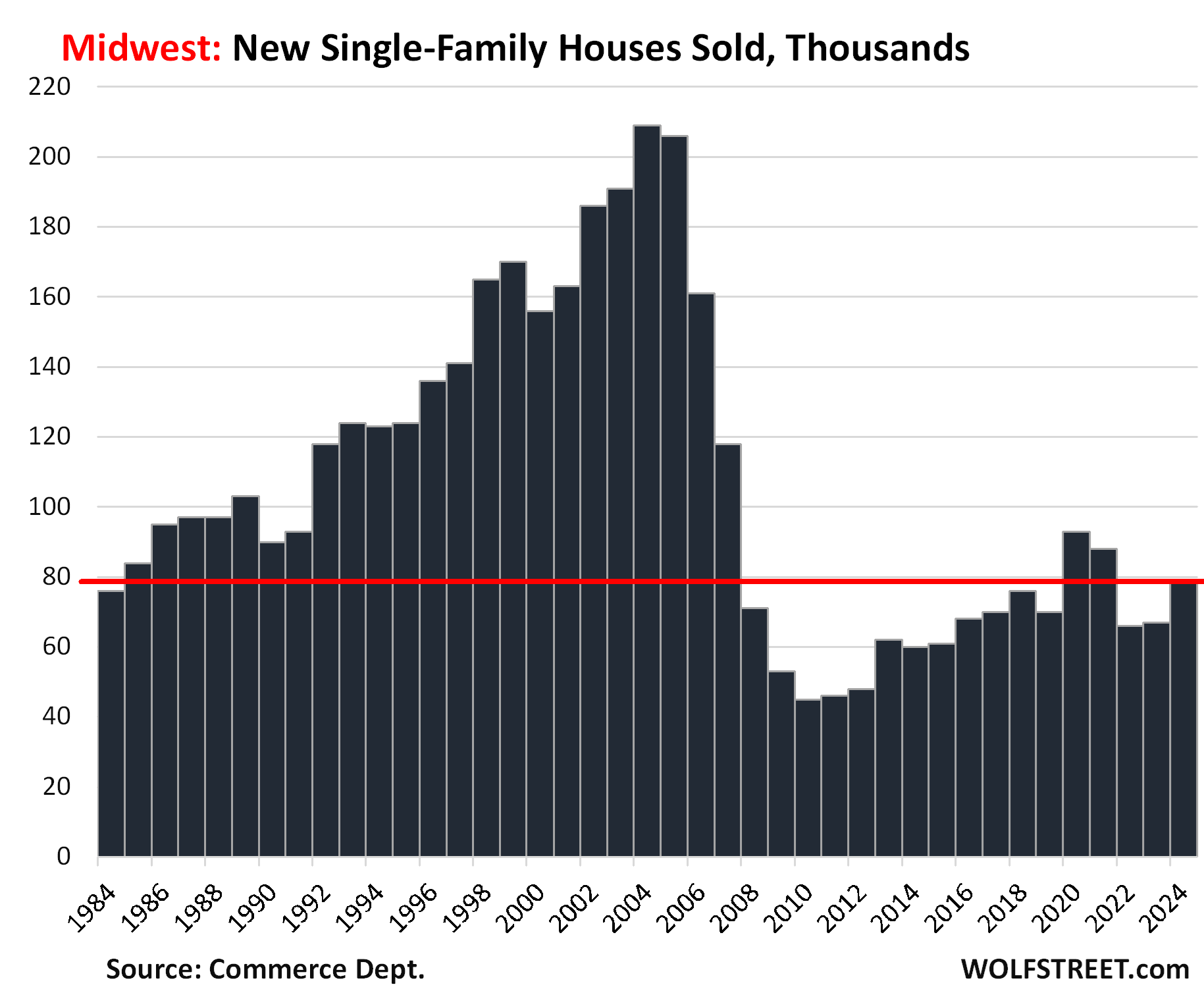

In the Midwest, sales of single-family houses in 2024 rose to 79,000:

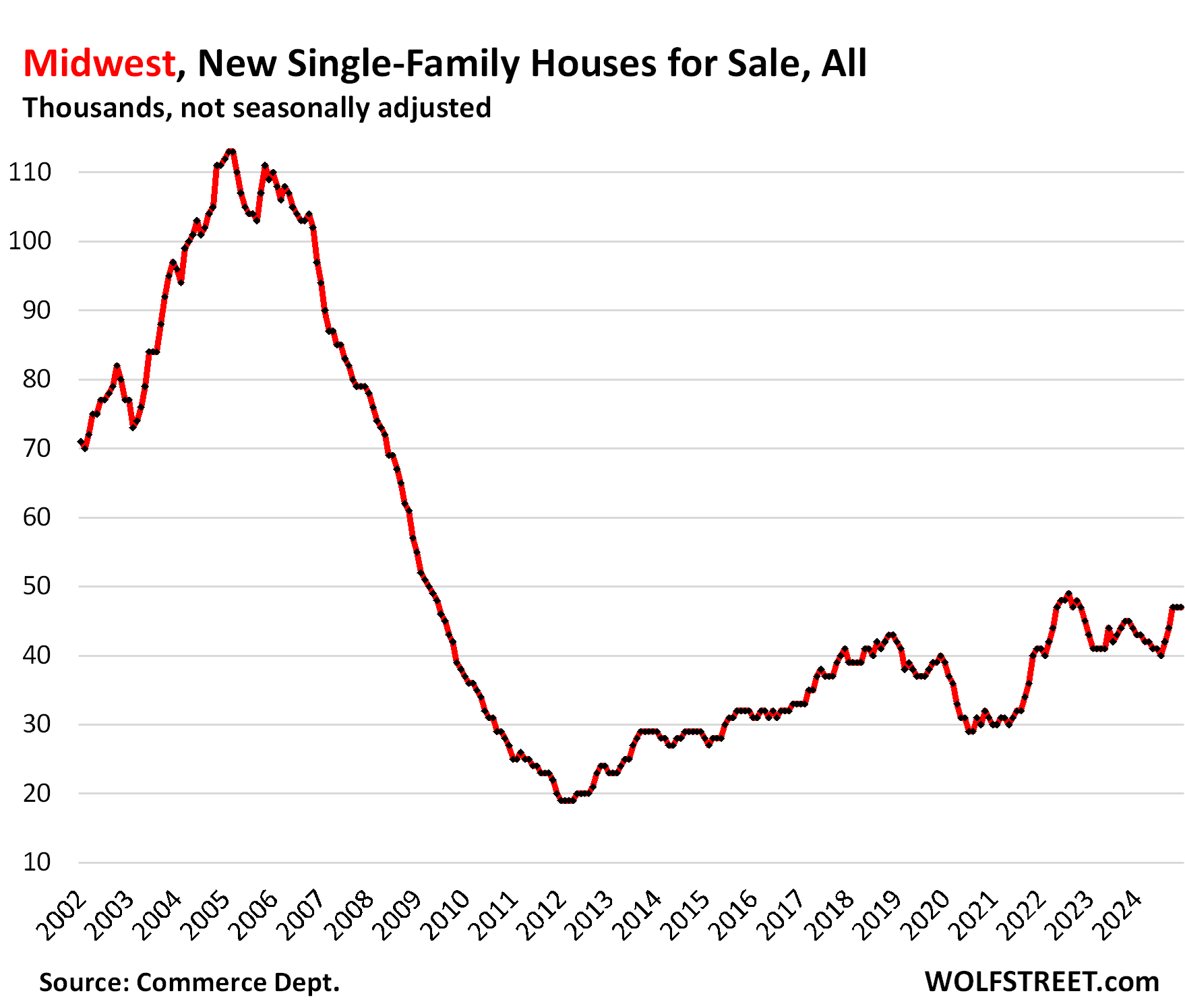

Inventory in the Midwest, at 47,000 houses over the past three months, is at the highest level since late 2022, and beyond that at the highest level since 2009. Supply exceeds 9 months on a three-month average basis.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()

The post Glut of New Houses for Sale in the South Is Bigger Even than during the Housing Bust. The Glut in the West Gets Close appeared first on Energy News Beat.

“}]]