[[{“value”:”

[[{“value”:”

The surge of the “nontraditional reserve currencies.”

By Wolf Richter for WOLF STREET.

The status of the US dollar as the dominant global reserve currency has helped the US fund its twin deficits, and thereby has enabled them: the huge fiscal deficit every year and the massive trade deficit every year. The reserve currency status comes from other central banks (not the Fed) having purchased trillions of USD-denominated assets such as Treasury securities, other government securities, corporate bonds, and even stocks. The dollar status as the dominant reserve currency has been crucial for the US, and as that dominance declines ever so slowly, risks pile up ever so slowly.

The US dollar lost further ground as top global reserve currency in 2024, according to the IMF’s COFER data released today. Total holdings of USD-denominated securities by other central banks (not the Fed) fell by $59 billion to $6.63 trillion at the end of 2024, from $6.69 trillion at the end of 2023.

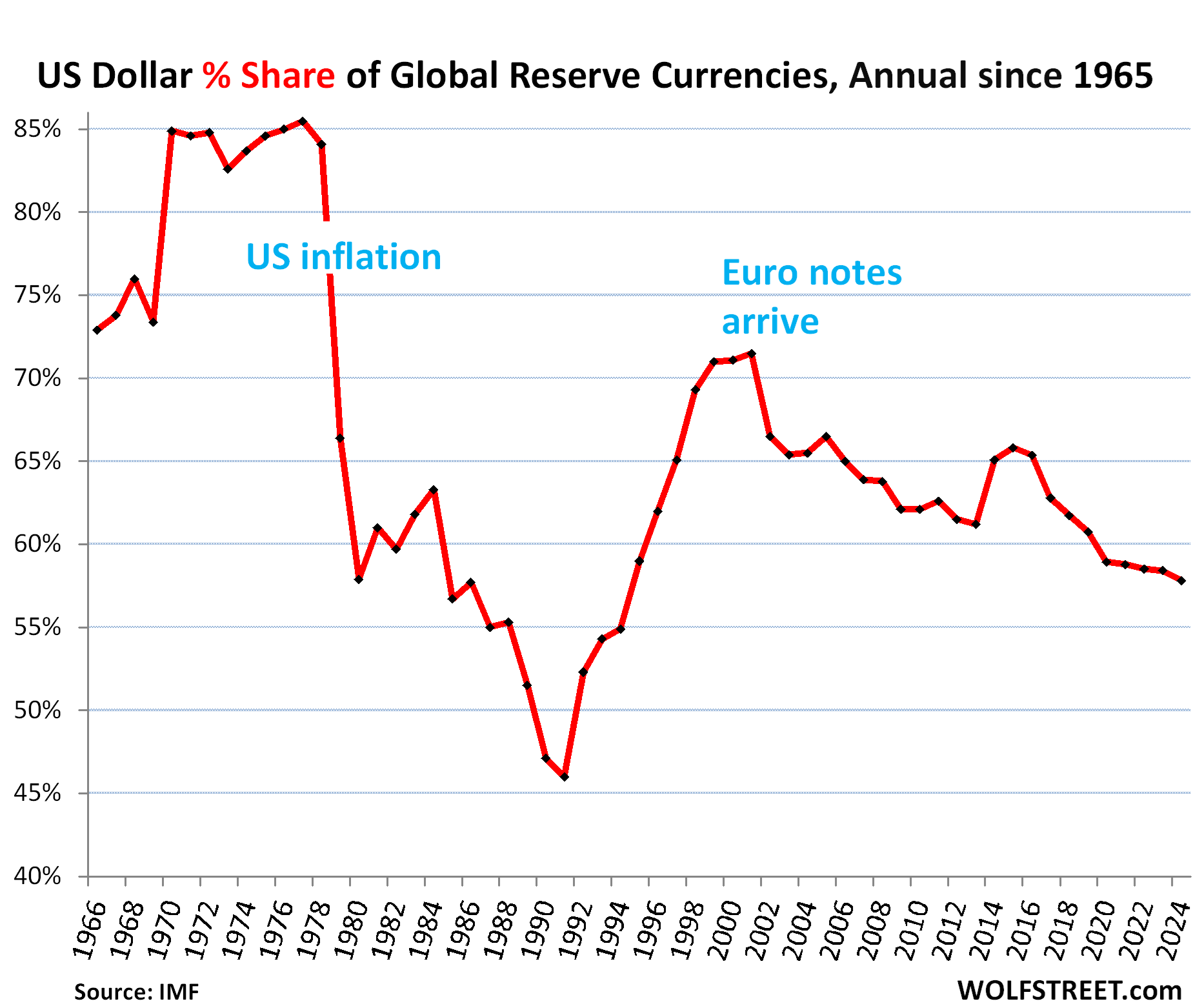

And the dollar’s share declined to 57.8% of total allocated exchange reserves at the end of 2024, the lowest since 1994, down by 7.3 percentage points in 10 years, as central banks have been diversifying their holdings for years to assets denominated in currencies other than the dollar, and into gold.

The dollar had already experienced a huge loss of global confidence before: Its share plunged from 85% in 1977 to a share of 46% in 1991, after inflation had exploded in the US in the 1970s and early 1980s. But by the 1990s, as inflation had been brought down and mostly stayed down, central banks loaded up on USD-assets again, and the dollar regained share as a reserve currency until the euro became a full-fledged currency.

USD-denominated foreign exchange reserves include US Treasury securities, US agency securities, US MBS, US corporate bonds, US stocks, and other USD-denominated assets held by central banks other than the Fed.

The major reserve currencies.

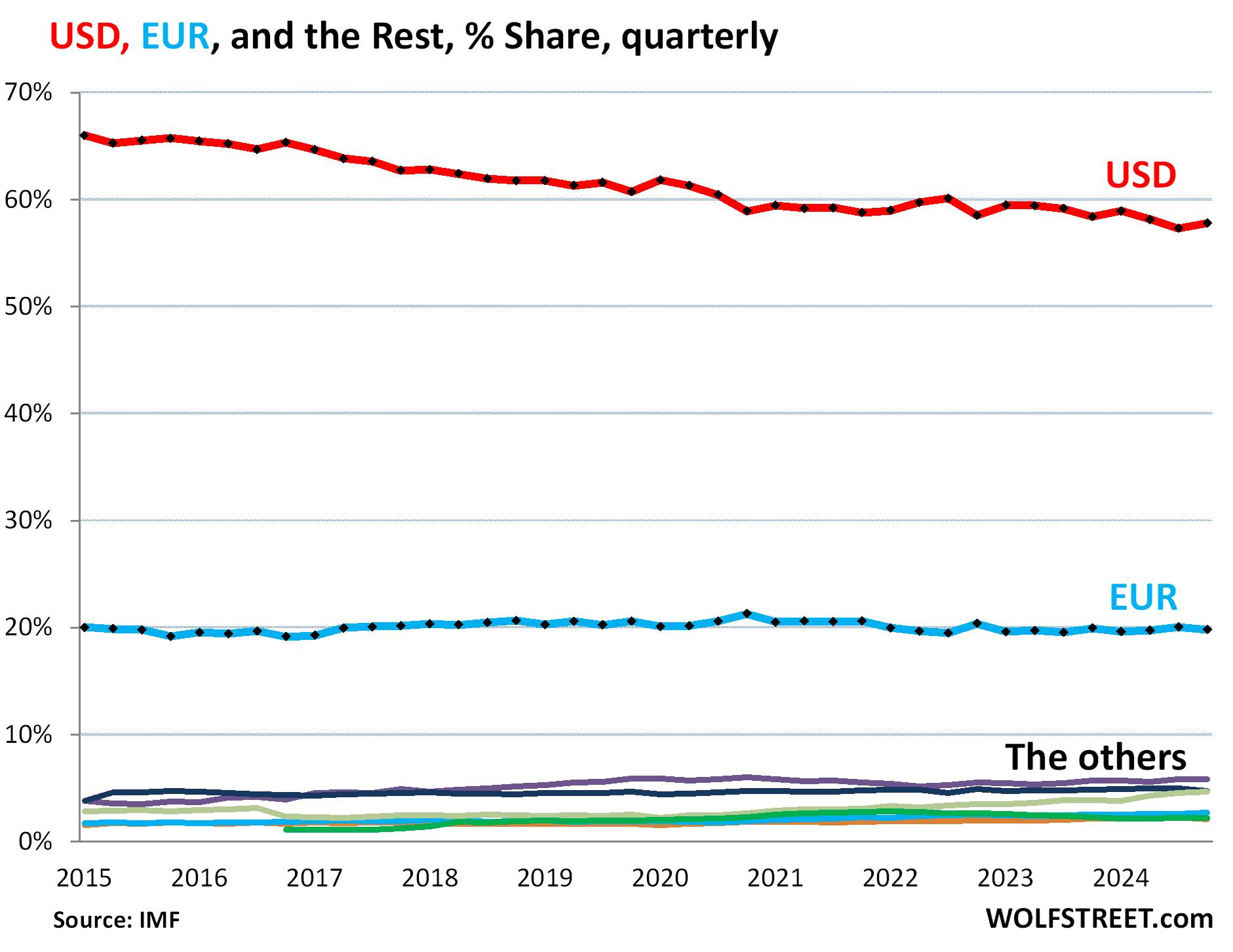

Central banks holdings of foreign exchange reserves denominated in all currencies, including in USD, edged up in 2024 to $12.36 trillion (from $12.35 trillion at the end of 2023).

Excluded from the total are any central bank’s assets denominated in its own currency, such as the Fed’s holdings of Treasury securities and MBS, the ECB’s holdings of euro-denominated bonds, and the Bank of Japan’s holdings of yen-denominated assets.

The USD is not losing share to the euro. The euro has been the #2 global reserve currency, with holdings at $2.27 trillion at the end of 2024. Its share has been around 20% for years, with a low of 19.1% in 2016 and a high of 21.3% in 2020. In Q4, the euro’s share was 19.8% (blue in the chart below).

So over the years, the USD has not lost share to the euro; it lost share to other reserve currencies, including “nontraditional reserve currencies,” as the IMF calls them. The colorful tangle at the bottom of the chart represents the largest of these other reserve currencies. More on those in a moment.

The surge of the “nontraditional reserve currencies.”

Some of these other reserve currencies have been gaining share at the expense of the dollar, especially the currencies in the basket of the “nontraditional reserve currencies,” that the IMF combines into “All others,” whose combined share has been surging since 2020 (red in the chart below).

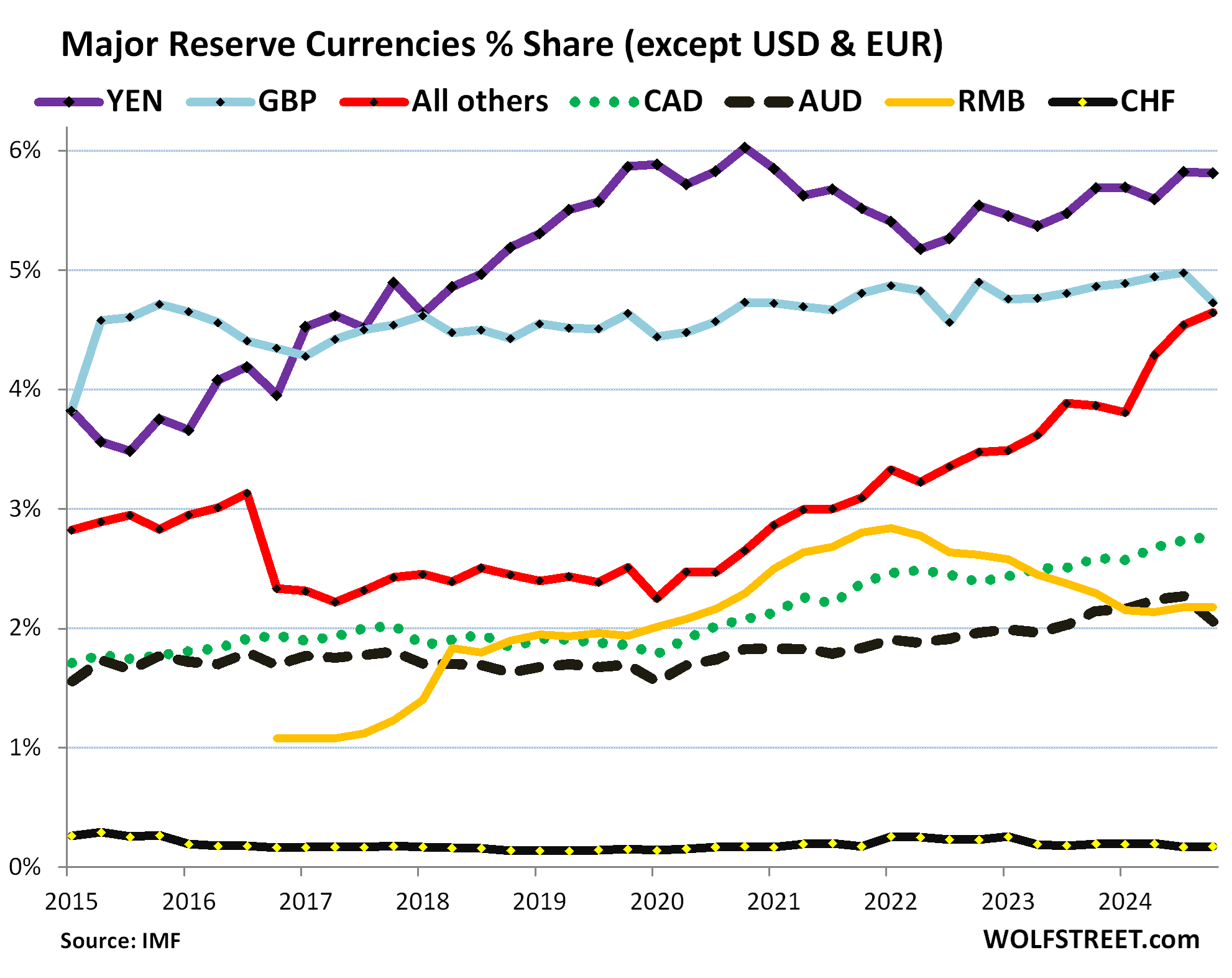

But the Chinese renminbi has lost share. China is the second largest economy in the world, but its currency, the renminbi, plays only a small role as a reserve currency. And it has lost ground against the USD and other currencies since 2022. Central banks have not been enamored with RMB-denominated assets due to China’s capital controls, the RMB’s convertibility issues, and other complexities (yellow line).

Note the surge of the nontraditional reserve currencies combined in the “all other currencies” group (yellow).

- Japanese yen, 5.8% (YEN, purple).

- British pound, 4.7% (GBP, light blue).

- “All other currencies,” 4.6% (red).

- Canadian dollar, 2.8% (dotted green).

- Chinese renminbi, 2.2% (yellow).

- Australian dollar, 2.1% (black dotted).

- Swiss franc, 0.2% (black).

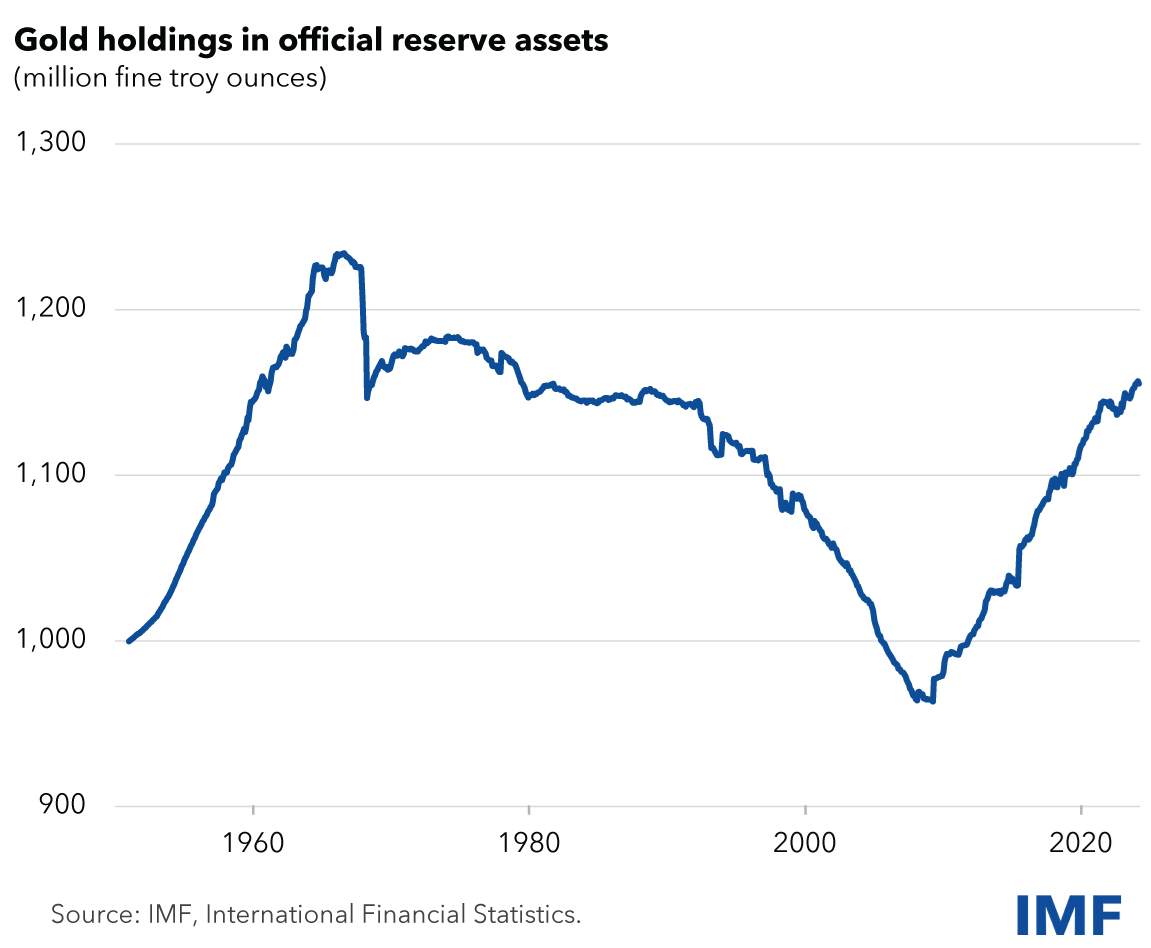

The other diversification: gold.

Gold bullion is not a “foreign exchange reserve” asset of central banks and is not included in the data above. Gold is a “reserve asset” not involving foreign exchange.

After four decades of unloading their gold holdings, central banks started re-adding gold about 20 years ago.

The top four holders have not changed their gold holdings in at least 20 years (based on IMF data released by the World Gold Council):

- US: 8,133 tonnes

- Germany: 3,352 tonnes

- Italy: 2,452 tonnes

- France: 2,437

But there has been a lot of movement below the top four, especially with Russia and China, which are now the #5 and #6 largest holders. And they did move the needle:

- Russia: 2,333 tonnes, little changed since Q2 2022. But between 2005 and 2022, Russia, one of the largest gold producers, had added nearly 2,000 tonnes.

- China: 2,280 tonnes. In 2024, it added 44 tonnes. It started piling on gold in 2009 and by 2015 had tripled its holdings

Since 2005, Russia and China combined have added 3,626 tonnes to their holdings.

Smaller holders have added large amounts of gold in 2024, such as Poland, India, Kyrgyzstan, Uzbekistan.

According to the IMF figures not updated for 2024, central banks’ gold holdings have surged by roughly 200 million troy ounces (6,221 tonnes) from 2006 to 1.16 billion troy ounces, driven largely by China and Russia. The increases in China and Russia alone represent nearly 60% of the total increase since 2006.

In dollar terms, these gold holdings at today’s price amount to $3.65 trillion. The IMF’s chart has not been updated for 2024, but it shows the historic moves:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Status of US Dollar as Global Reserve Currency: Central Banks Diversify into Other Currencies and Gold appeared first on Energy News Beat.

“}]]