[[{“value”:”

[[{“value”:”

Something rare occurred: Auto loan balances fell despite highest new & used vehicle sales in years. More people paid cash to dodge interest rates?

By Wolf Richter for WOLF STREET.

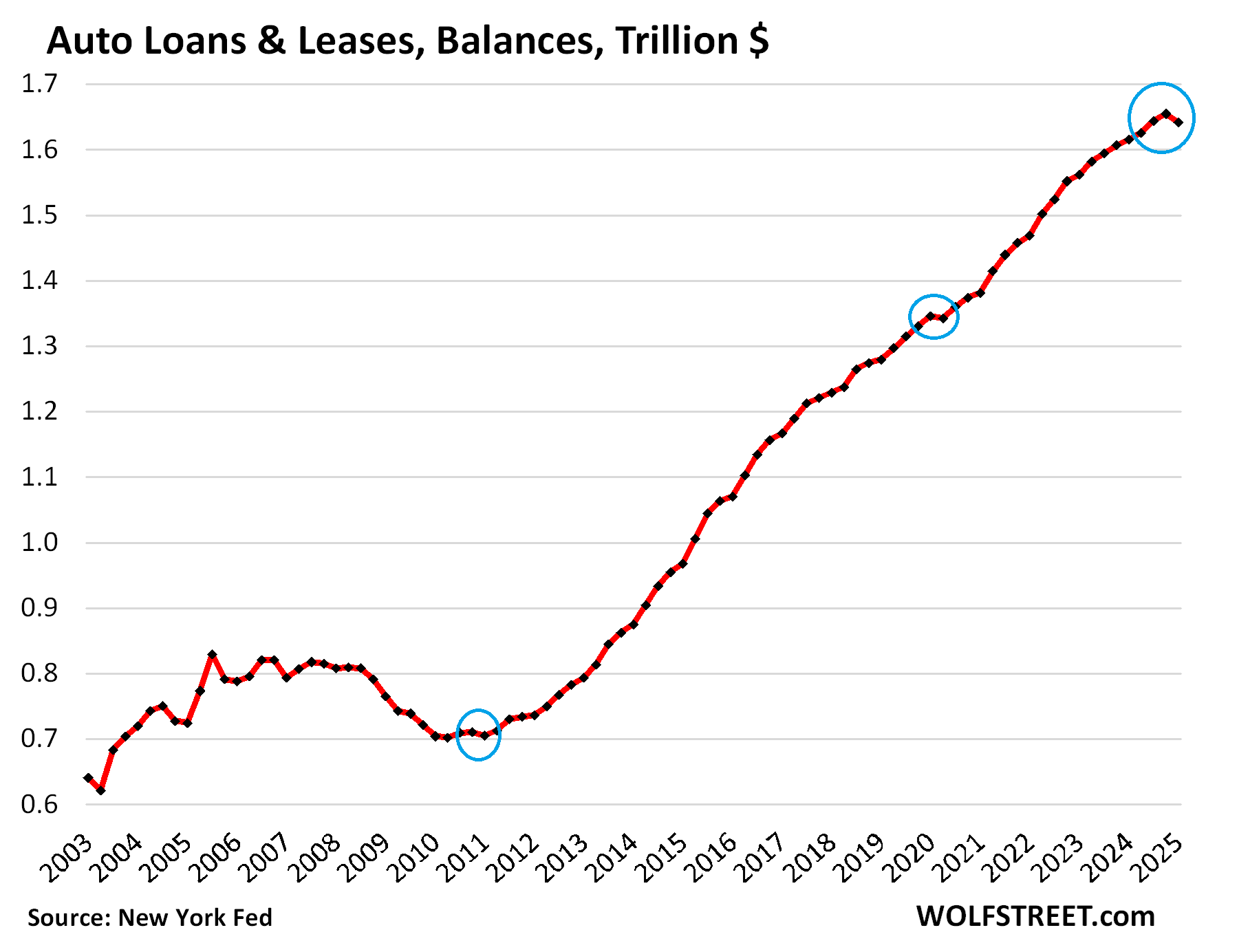

Total balances of auto loans and leases for new and used vehicles fell by $13 billion, or by 0.8%, in Q1 from Q4, the first quarter-to-quarter decline since Q1 2020, and only the second since Q1 2010 just after the Great Recession, according to the New York Fed’s report on consumer credit.

The prior two times, auto loan balances declined because in Q1 2020, sales plunged by 12.8% year-over-year; and Q1 2010 followed a 35% collapse of new-vehicle sales in 2008 and 2009 and was the final quarter of a big decline in auto loan balances.

But this time, loan balances declined despite strong demand: New vehicles sales booked the best Q1 since 2019, and used vehicle sales booked the best Q1 in years. Maybe a sign of strength: Lots of used-vehicle buyers pay cash. And the share of cash buyers has been rising (to dodge the interest rates?), reaching 63.5% in Q4, from 61.3% a year earlier, and from 58.4% two years earlier, according to Experian.

The burden of auto loans and leases.

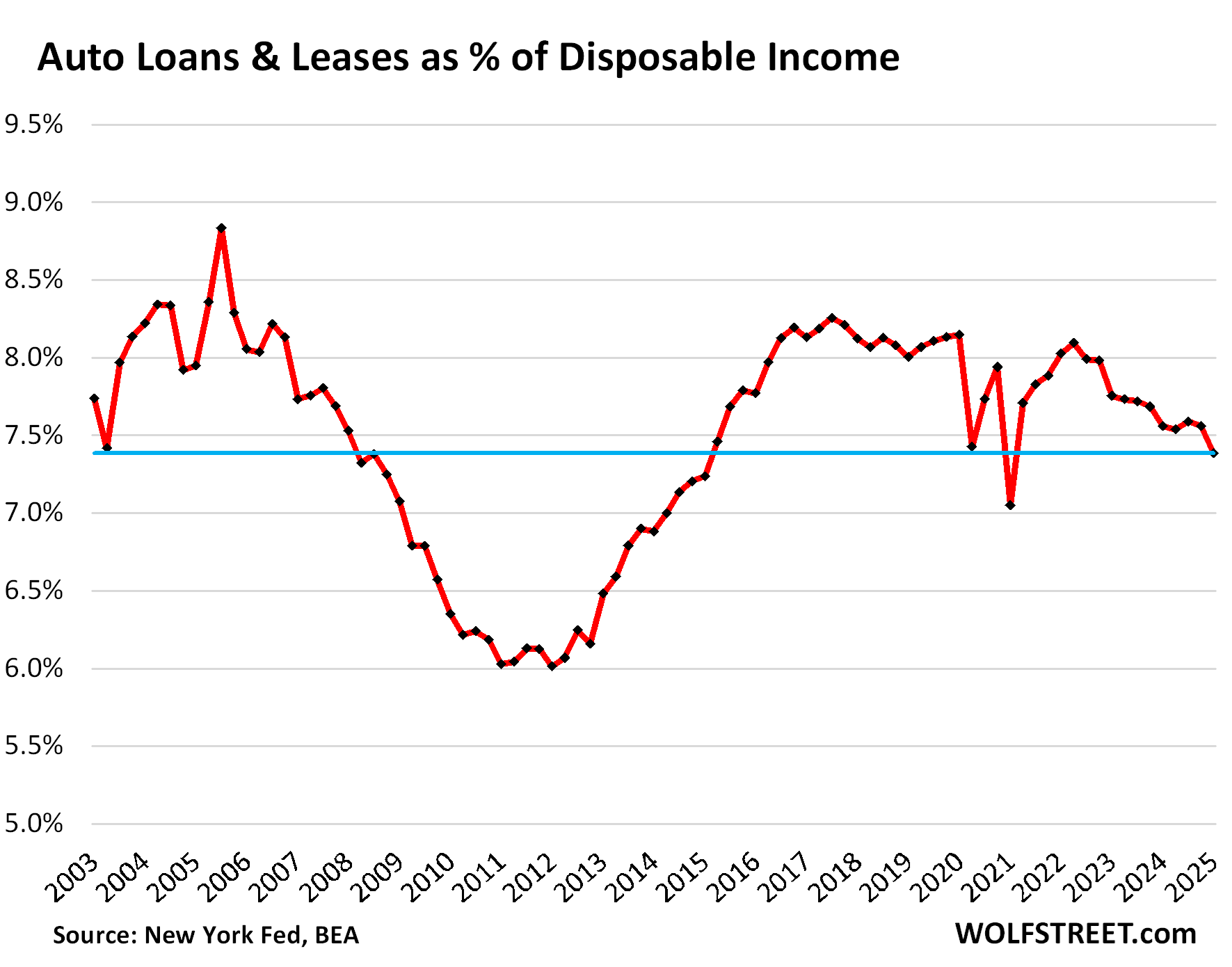

Debt-to-income ratios and debt-to-cash-flow ratios are classic measures of borrowers’ ability to deal with the burden of their debt. With households, a metric of cash flow is “disposable income,” which represents the cash households have available, after payroll taxes, to spend on housing, debt payments, food, fuel, and other expenses.

Disposable income is household income from all sources except capital gains, minus payroll taxes: So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

Disposable income rises with higher incomes at individual households and with more people working and making money (population/job growth):

- QoQ: disposable income +1.6%, auto debt: -0.8%.

- YoY: disposable income +4.0%, auto debt: +2.6%.

Due to the decline in auto loan balances in Q1 and the increase in disposable income, the debt-to-income ratio fell (improved) to 7.4%:

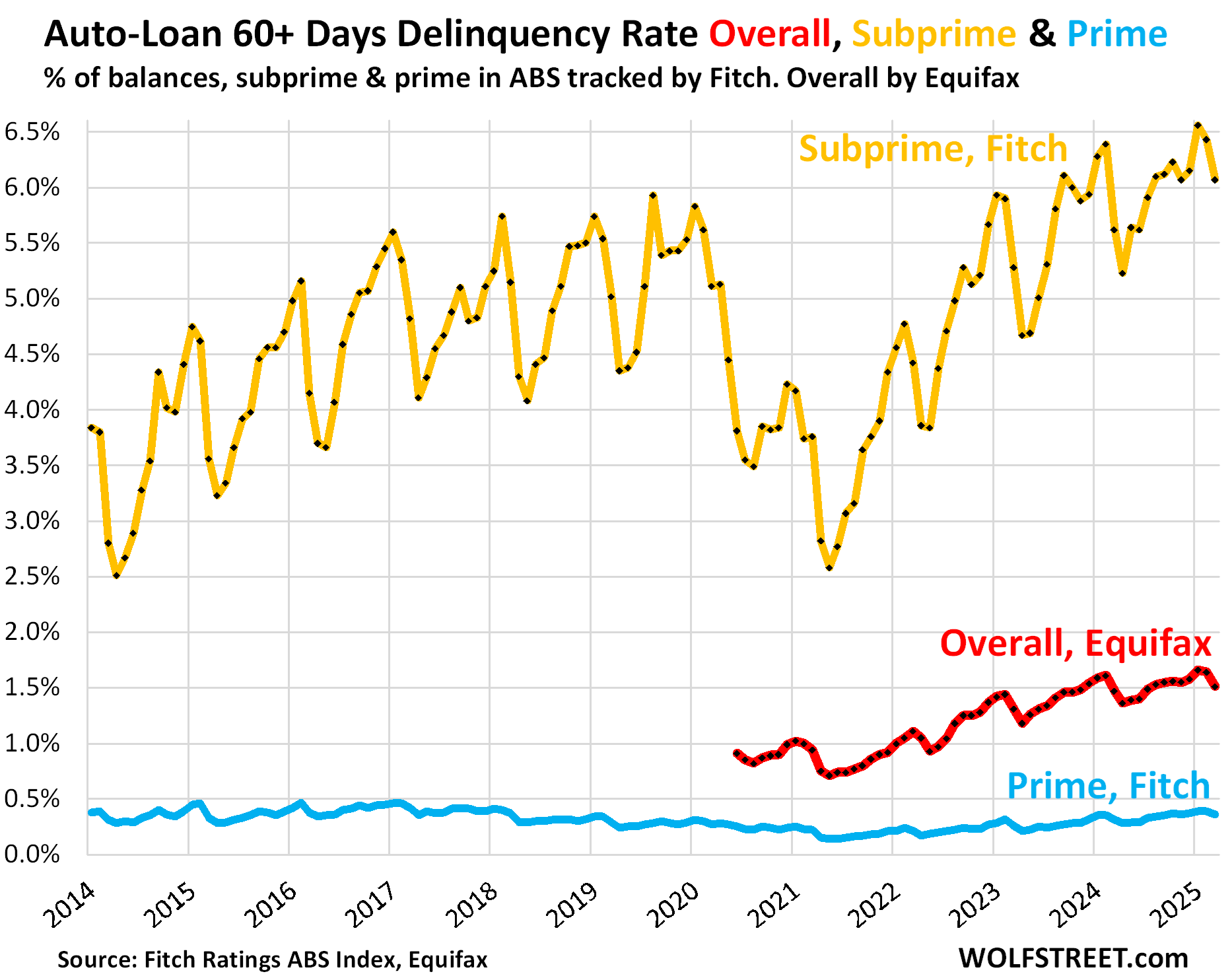

Serious delinquency rates: total, subprime, and prime.

The 60-plus day delinquency rate for all auto loans and leases fell to 1.51% in March, from 1.64% in February and 1.66% in January, per Equifax data. Compared to a year ago, it was up a hair (1.47% in March 2024), and the difference would have gotten lost in rounding to 1.5%. During the Free-Money era of the pandemic, delinquency rates had dropped below 1% (red in the chart below).

Subprime is always in trouble which is why it’s “subprime.” Fitch, which rates asset-backed securities (ABS) backed by auto loans, publishes the delinquency rates for auto loans that are prime-rated at the time of origination (blue in the chart below) and auto loans that are subprime-rated at origination (gold in the chart below).

Fitch’s subprime 60-day-plus delinquency rate declined to 6.07% in March along seasonal patterns (peaks in January or February). Compared to a year ago, it was 45 basis points higher.

Of all loans and leases outstanding, only 14.1% were subprime and deep-subprime rated at origination, according to Experian data.

Nearly all subprime auto loans financed the purchase of used vehicles, mostly older used vehicles sold by specialized subprime dealer-lender chains, or financed by specialized subprime lenders. Lenders package these subprime auto loans into ABS and sell these bonds to pension funds and other institutional investors that buy them for their higher yield. It’s a small specialized high-risk-high-profit part of auto lending. When losses occur, they’re spread across investors that got paid to take those losses, not banks.

Subprime means “bad credit” at the time of origination – a history of being late in paying obligations, or not paying them at all. It does not mean “low income.” Low-income people have trouble borrowing, and if they can get credit at all, the amounts are small. It’s people with high-enough incomes that get seriously into it over their head, often as part of a learning experience.

Prime-rated auto loans are in pristine condition. In March, the delinquency rate of loans that had been rated prime at the time of origination dropped to 0.36%. Even during the Great Recession, the prime delinquency rate maxed out at only 0.9% (blue).

So overall, auto loans are in good shape, with the small segment of subprime borrowers – a high-risk-high-profit business – always being in trouble except when the free money temporarily lowered the risks and increased the profits and the recklessness in the industry. Since the free money ended, a number of the PE-firm-owned specialized subprime dealer-lender chains have collapsed. And the biggie in the subprime dealer-lender industry, publicly traded America’s Car-Mart [CRMT], ran into trouble, and its shares have plunged by 70%. But that comes with high-risk-high-profit activities.

In terms of our Drunken Sailors, as we’ve come to call them lovingly and facetiously, the vast majority of them is handling their auto loans – those that don’t pay cash for their cars – just fine.

In case you missed the earlier parts of the debts of our Drunken Sailors:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post Auto-Loan Balances, Debt-to-Income Ratio, Serious Delinquencies for Subprime & Prime in Q1 2025: Our Drunken Sailors and their Auto Loans appeared first on Energy News Beat.

“}]]