[[{“value”:”

[[{“value”:”

Will the bond market eventually wake up and scare the bejesus out of Congress? Is it already rubbing its eyes?

By Wolf Richter for WOLF STREET.

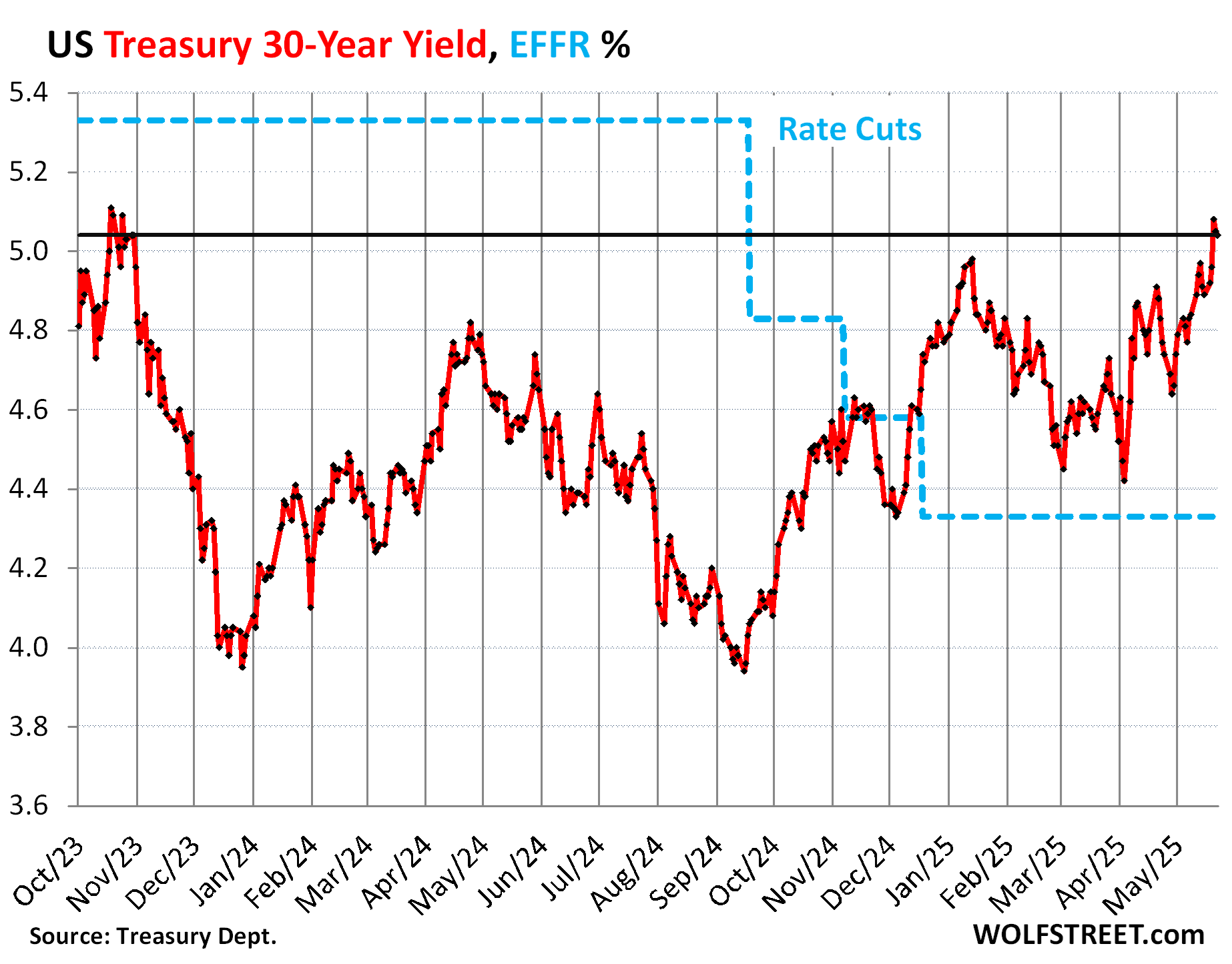

The 30-year Treasury yield ended Friday at 5.04%, after kissing 5.15% on Thursday. These above-5% yields are the highest since the debt-scare in October 2023. The 20-year yield has also been above 5% for the last three days of the week.

The Fed started cutting its policy rates in mid-September 2024, by a total of 100 basis points so far. The Effective Federal Funds Rate, which the Fed targets with its policy rates, has dropped by 100 basis points, from 5.33% to 4.33% (blue line in the chart).

But over the same period since mid-September, the 30-year yield has surged by 110 basis points, in a spectacular counter-move (red in the chart). The gyrations around “Liberation Day” now look just like some additional squiggles in a longer up-trend.

When bond yields rise, bond prices fall. With bonds that have many years left to run, prices fall a lot when yields rise, which makes them risky in terms of market price, and “bond bloodbath” once again made the rounds in the financial media.

But for future buyers, higher yields and lower prices are appealing, and those future buyers are sitting there on their hands, licking their chops. Someday, when yields get high enough, they’re going to buy. When too many of these folks or algos are just licking their chops and waiting for even higher yields, instead of jumping in and buying now, that’s what causes yields to rise.

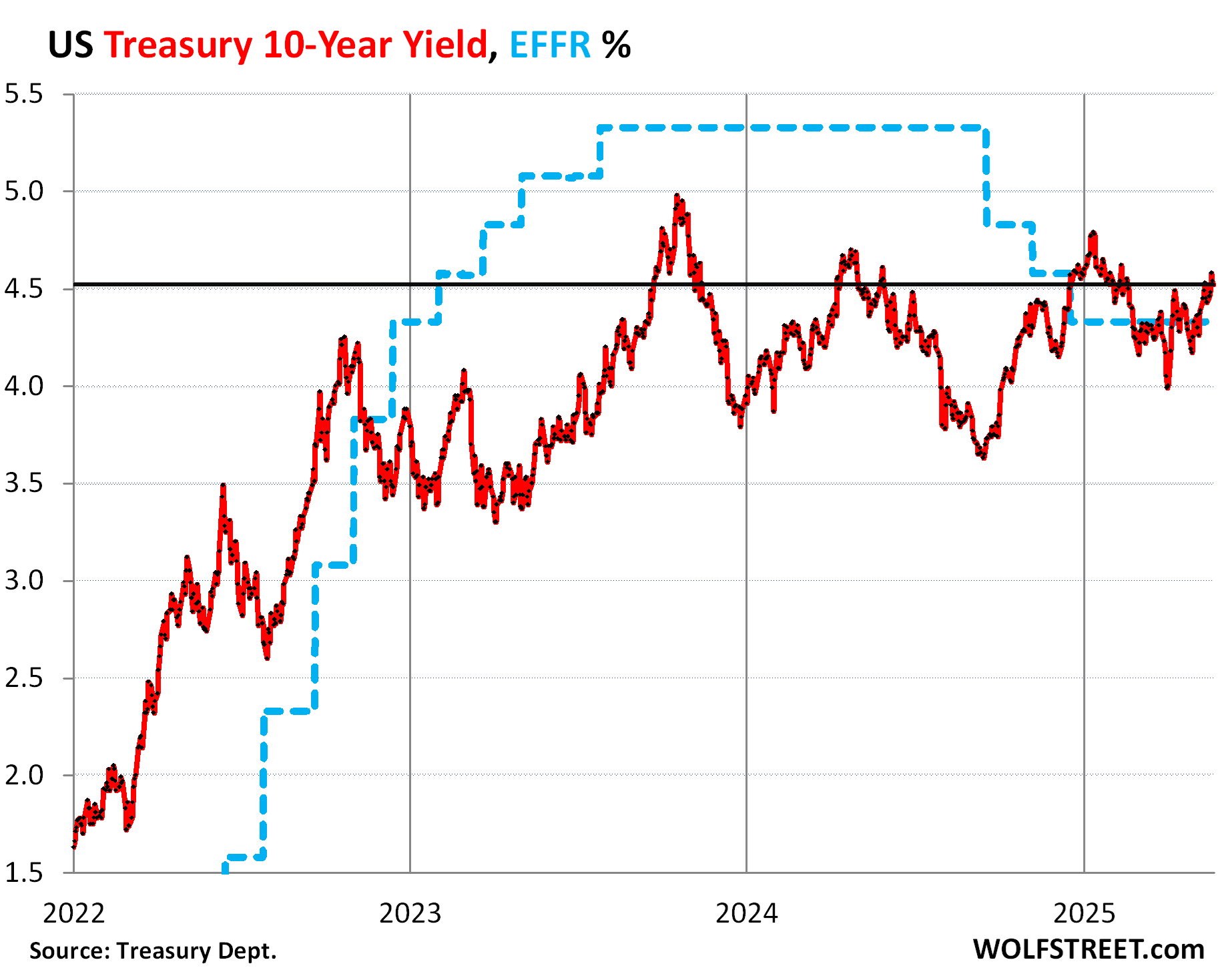

The 10-year Treasury yield ended Friday at 4.52%, after briefly kissing 4.61% on Thursday. So it’s back where it had been in February.

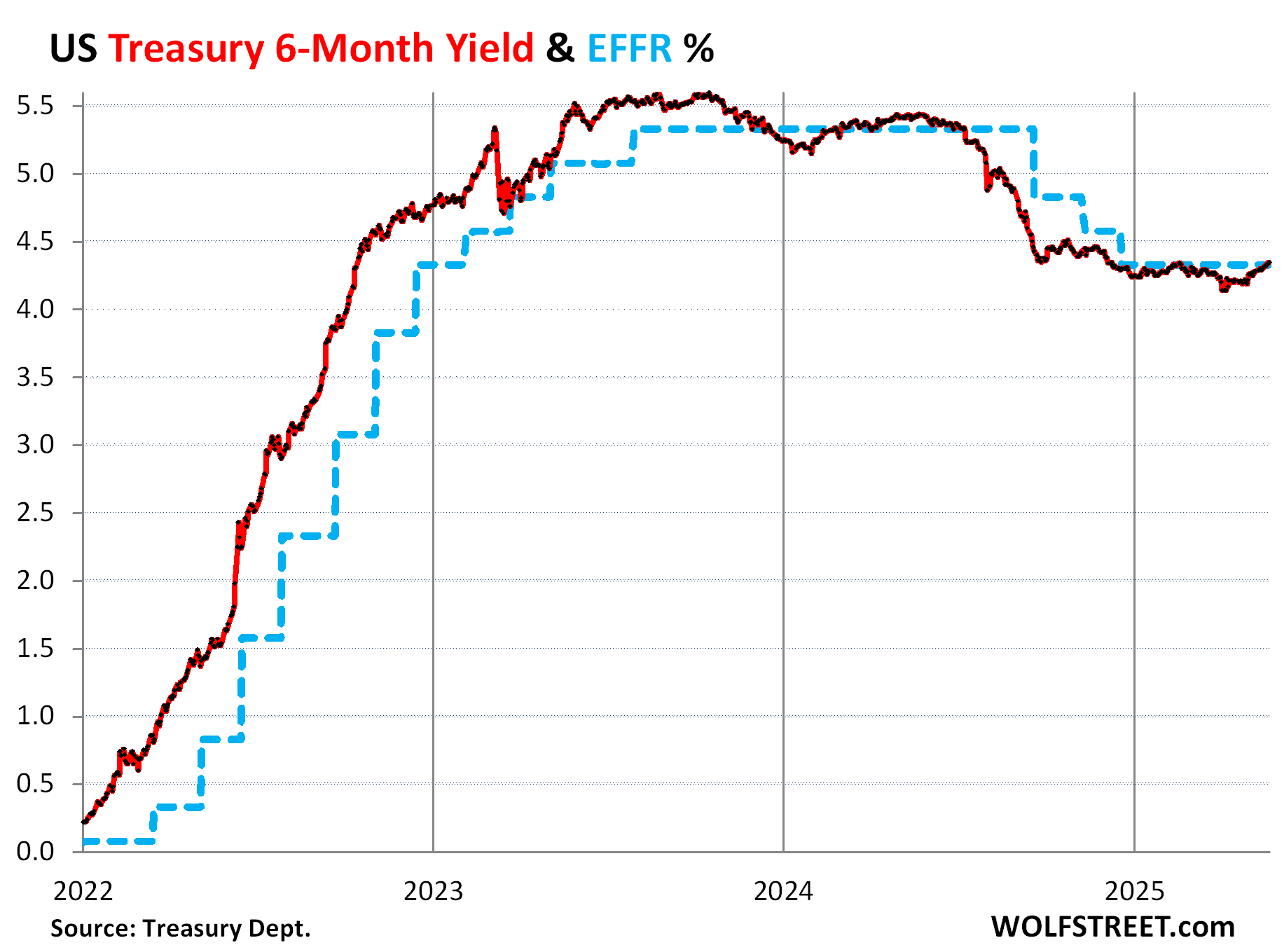

No rate cut for months: 6-month Treasury yield.

The six-month Treasury yield has taken rate cuts off the table within its window which extends to about three to four months. It normally does a pretty good job of anticipating rate hikes and cuts months in advance, as market participants listen to every comma the Fed utters or fails to utter.

It has ticked up by 20 basis points since early April and now hovers right at the EFFR, amid persistent chanting by the Fed and Fed governors of the wait-and-see mantra.

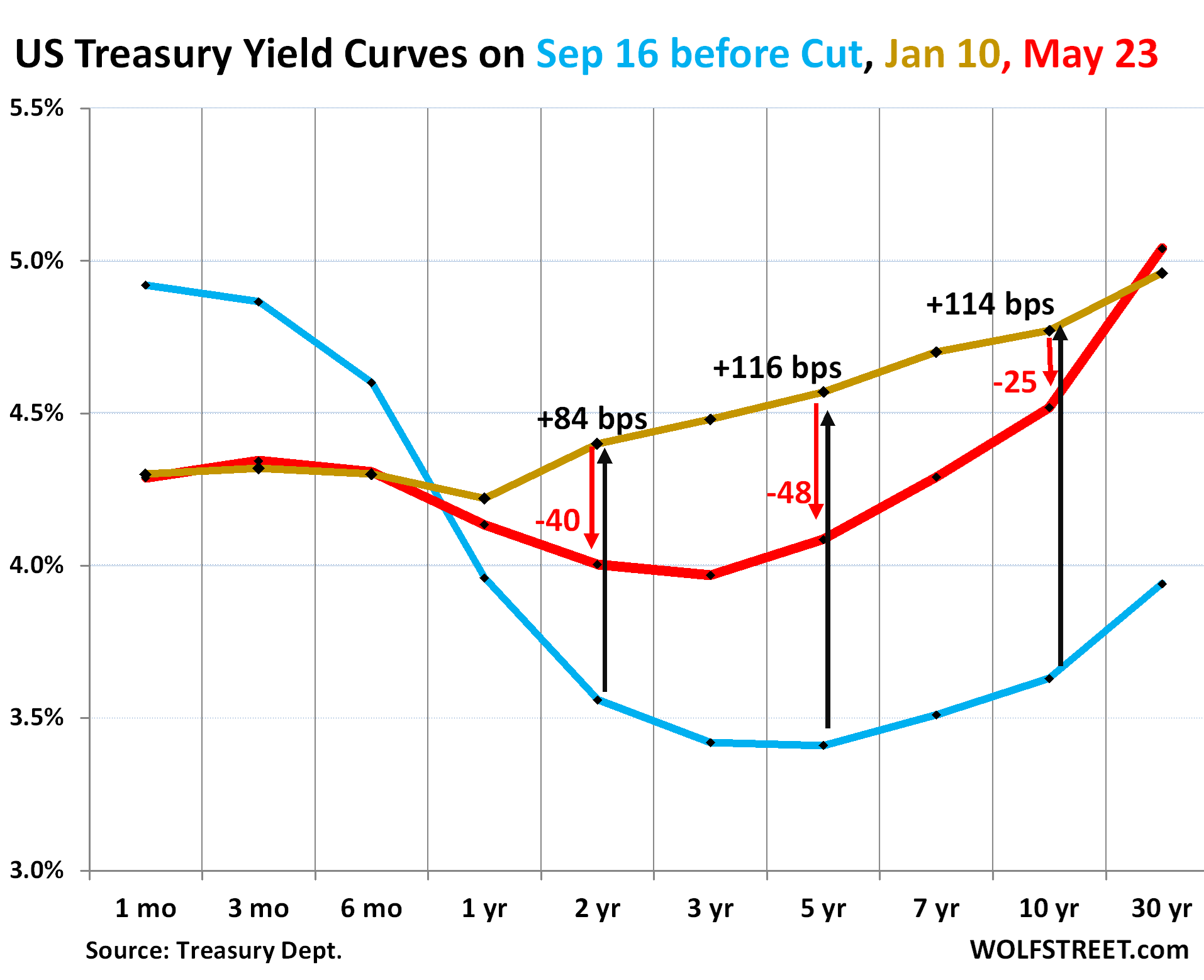

Yield curve steepened at long end, sag in the middle flattened.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: January 10, 2025, just before the Fed pivoted to wait-and-see.

- Red: Friday, May 23, 2025.

- Blue: September 16, 2024, just before the Fed’s monster rate cut.

The 30-year yield has snapped back and is now above where it had been on January 10. The 10-year yield is only 25 basis points from where it had been on January 10. The 7-year yield is right where the short-term yields are. Everything longer than the 7 years is now above short-term yields and that part of the yield curve has fully re-un-inverted, so to speak.

And the sag in the middle between the 6-month yield and the 7-year yield has gotten shallower in recent weeks as those yields have risen.

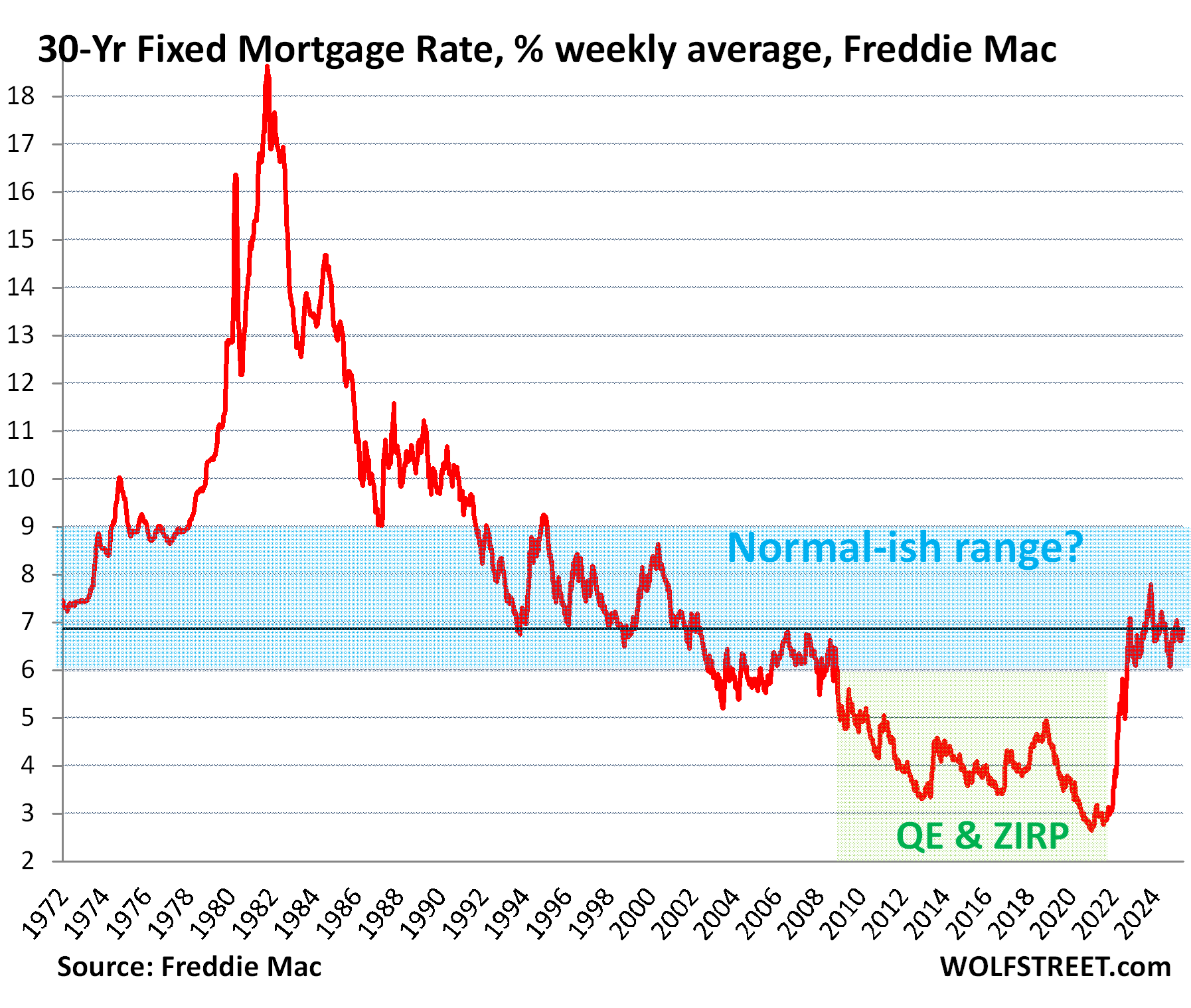

Mortgage rates again above 7%.

The average 30-year fixed mortgage rate has been once again above 7% for the last three days of the week, and right at 7% for the first two days of the week, according to Mortgage News Daily. It went over 7% for the first time in this cycle at the end of September 2022. The once unthinkable 7% mortgages have become the new normal? But they were the old normal, sort of.

By Freddie Mac’s measure on Thursday, the average mortgage rate for the week through Wednesday rose to 6.86%. This measure has been north of 6% since September 2022, and between 6.5% and 7.5% much of the time.

The average 30-year fixed mortgage rate didn’t drop to 5% until the Fed started QE in 2009, which included the purchases of ultimately trillions of dollars of mortgage-backed securities, which helped push down mortgage rates, ultimately below 3%, which triggered historic home price inflation. But in 2021, consumer-price inflation began to also rage, and the Fed eventually put an end to QE, and since mid-2022 has conducted QT, shedding by now $2.26 trillion in assets, including $570 billion in MBS.

The 3% mortgage rates were a brief aberration that created massive distortions in the already distorted US housing market and were the final act of the 40-year bond bull market.

Sleeping through the first innings of anathema.

For the people and algos that are waiting for higher yields before buying, the current yields, though up some, are still not a good deal.

At first it was the swirling fear of stubborn re-accelerating inflation and of a lax Fed: It cut 50 basis points last September just as inflation started to re-accelerate.

That fear is topped off by the fiscal mess: It appears likely that the Republican budget in the works will make the deficit even worse for years to come, increase debt issuance even more for years to come, thereby throwing more supply of debt on the market that then has to attract more buyers who need to be lured into the market with more attractive yields.

All three issues – fears of higher inflation, fears of a lax Fed, and additional years of unspeakable fiscal madness – are anathema for the bond market.

Except that the bond market has been sleeping through the first few innings of this anathema. It briefly woke up in the second half of 2023, but then dozed off again. And now it woke up again? Maybe just a little?

The last time the bond market was wide awake, nervously watching inning after inning of anathema, was in the late 1970s through the early 1990s, when the 10-year yield was mostly above 8%, and for some years much higher.

Eventually, the bond market scared the bejesus out of Congress and the White House, and they successfully trimmed the deficit. The bond market scaring the bejesus out of Congress and the White House for years to come – not just a brief episode that blows over – is likely the only force that can get them to trim the deficit. But that’s not happening right now.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post 30-Year & 20-Year Treasury Yields Back over 5%, 10-Year over 4.5%, Yield Curve Steepens at Long End, Mortgage Rates Back over 7% appeared first on Energy News Beat.

“}]]