[[{“value”:”

[[{“value”:”

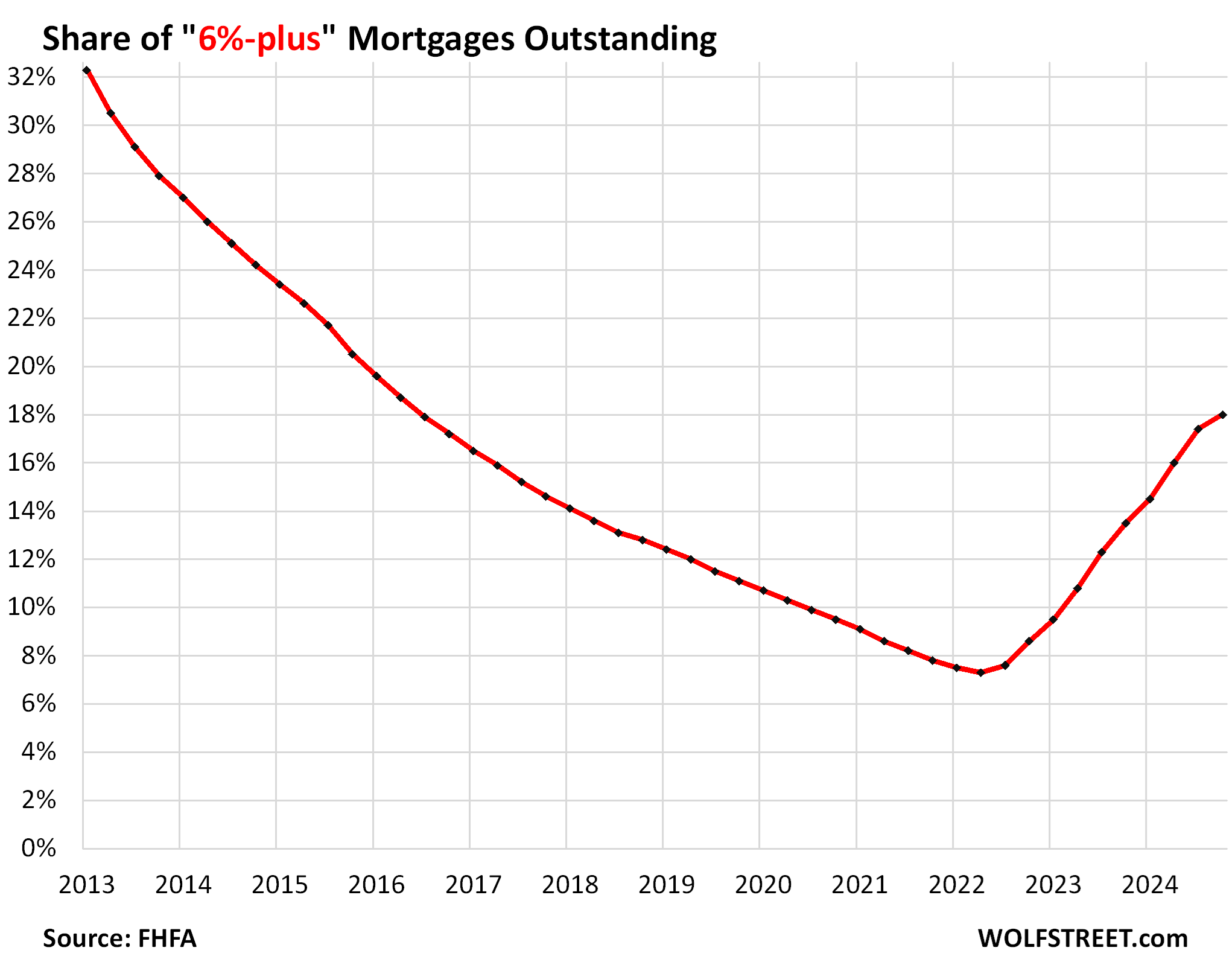

Conversely, the share of 6%-plus mortgages outstanding surges to the highest since 2016.

By Wolf Richter for WOLF STREET.

The 30-year mortgage with a fixed rate of 3% for the duration of 30 years was as close to free money in an inflationary world as regular folks can get, and it would make sense to hang on to it and never move and never refinance the mortgage and never do anything that would jeopardize this mortgage. But then life happens.

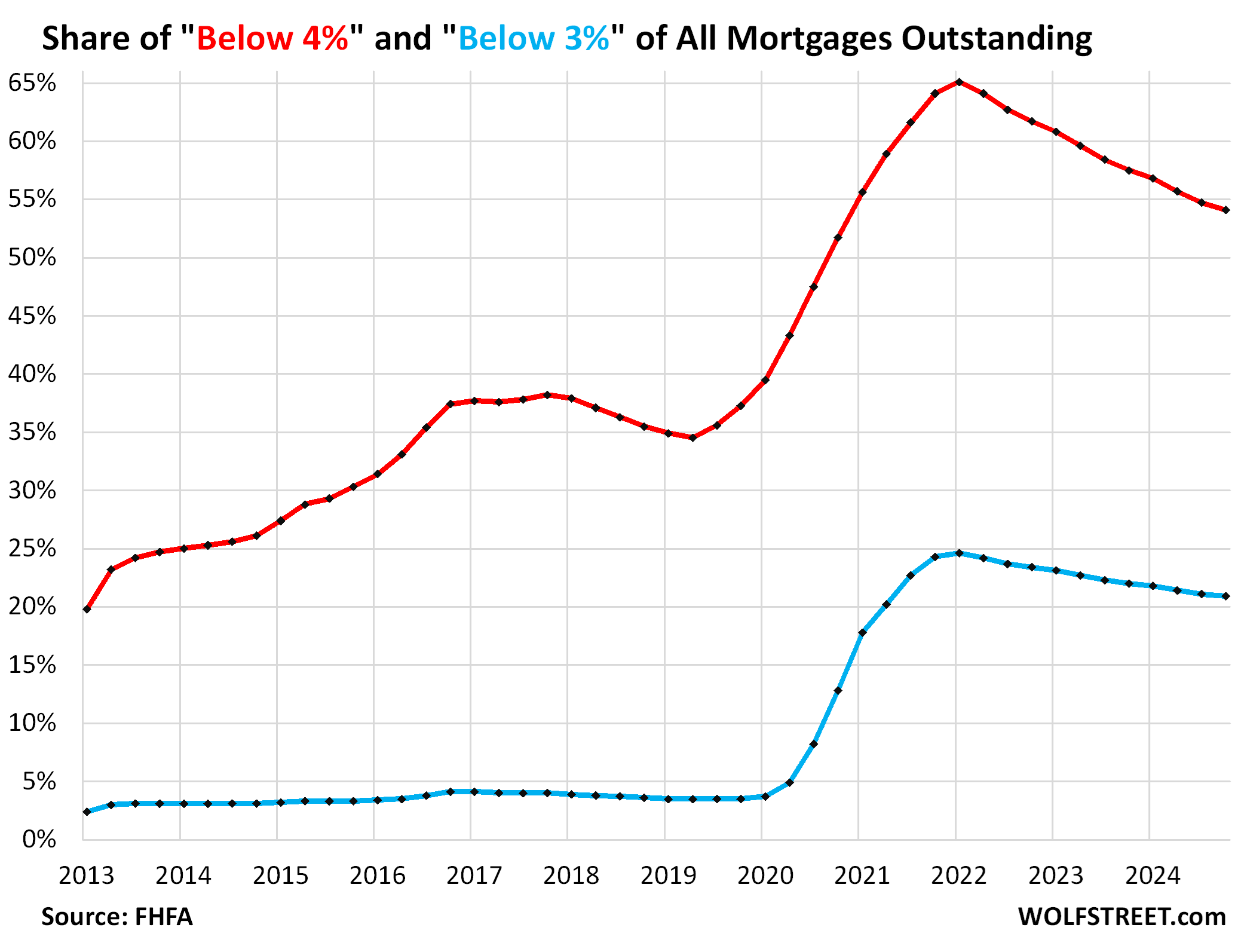

The number of mortgages outstanding with rates below 4% has been declining steadily as more and more of these mortgages get paid off. In Q4, the share dropped to 54.1% of all mortgages outstanding, the lowest since Q4 2020, and down from the high of 65.1% in Q1 2022 (red).

The share of mortgages outstanding with rates below 3% declined to 20.9% of all mortgages outstanding, the lowest since Q1 2021, and down from the peak in Q1 2022 of 24.6%, according to the Federal Housing Finance Authority’s National Mortgage Data Base on March 31 (blue in the chart below).

These mortgages include adjustable-rate mortgages, whose interest rates adjust based on some short-term benchmark interest rate, such as the six-month SOFR. Before there was SOFR, there was LIBOR. An ARM might be priced at 6-month SOFR plus a spread of 2 or 3 percentage points. During the years of ZIRP when the six-month SOFR/LIBOR was close to 0%, ARMs had very low rates, which explains the blue line before 2020.

But those homeowners experienced a payment shock when the Fed started hiking rates in 2022, and in July 2023, SOFR went over 5%, plus 2 or percentage points made for AMRs of 7% or 8%, up from 2%. That delivered a massive payment shock. Thankfully, not a lot of homeowners had ARMs.

Conversely, the share of 6%-plus mortgages outstanding rose 18.0% at the end of Q4 2024, the highest since Q2 2016, from a share of 7.3% at the low point in Q2 2022. It reflects purchase mortgages and refinance mortgages with rates of 6% or higher.

The fact that the share has more than doubled from 7.3% to 18% in a little over two years shows that “locked-in” ends when life happens: A change in jobs that requires a move, the need for a larger or smaller home, the urge to relocate closer to the kids. Death, divorce, marriage, natural disaster… are all reasons for 3% mortgages to get paid off. Other homeowners decide to sell the home to “lock in” their huge gains, pay off the mortgage, and walk away with piles of cash to invest, while paying rent instead of the costs of homeownership.

By historical measures, this share of 18.0% is still very low, as 30-year fixed rate mortgages were typically well above 6% in the decades prior to 2004.

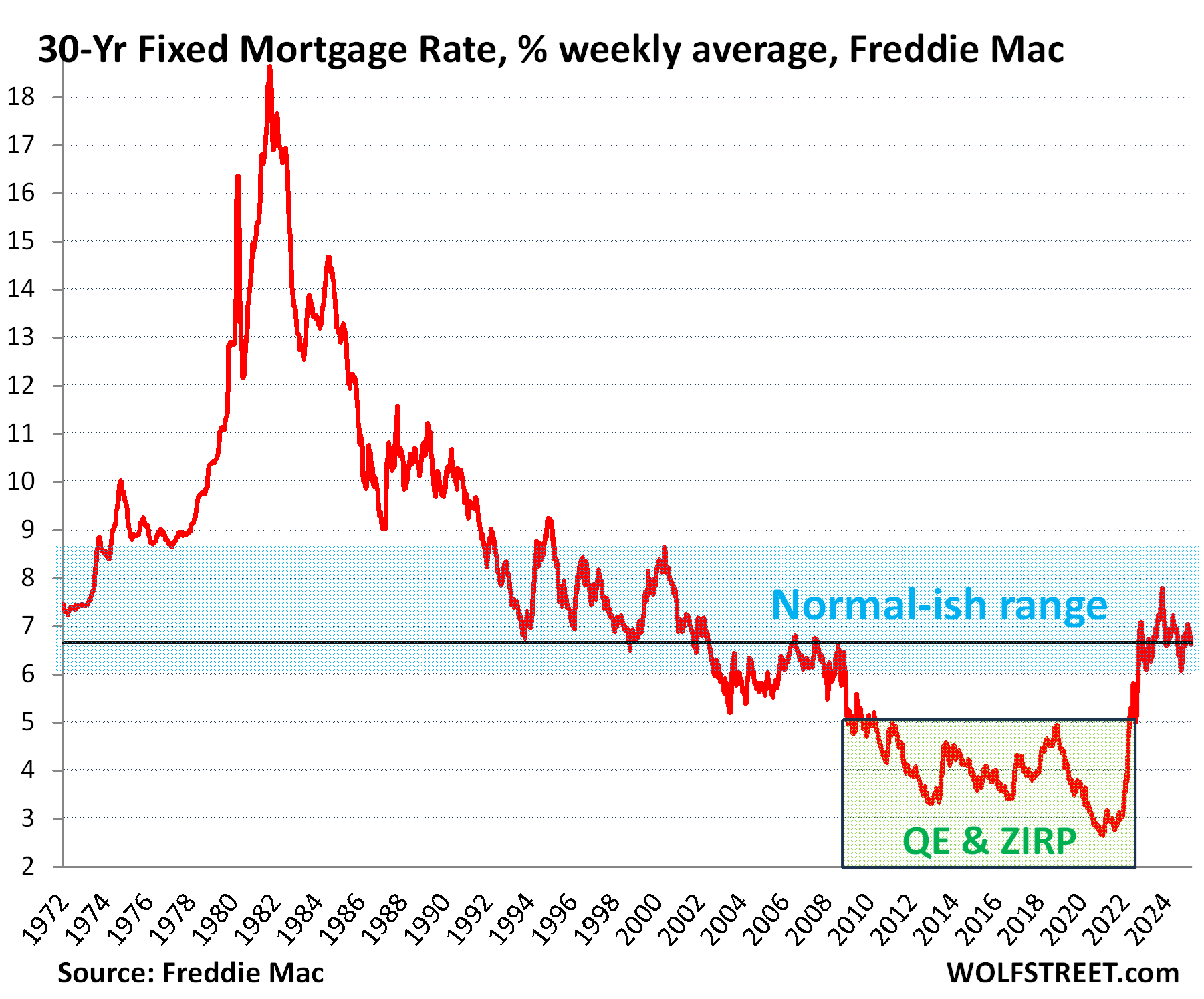

The average 30-year fixed mortgage rate has been above 6% since September 2022, according to Freddie Mac data.

The below-3% average 30-year fixed-rate mortgage occurred in a brief period from mid-2020 to late 2021, triggering the historic refinancing boom that by Q1 2022 caused nearly a quarter of all outstanding mortgages to have rates of less than 3%.

Below-4% mortgage rates occurred periodically starting in 2012.

Those super-low mortgage rates were a result of the Fed’s QE when the Fed bought bonds, including large volumes of mortgage-backed securities (MBS) specifically to repress mortgage rates, and those repressed mortgage rates caused home prices to explode, which is now the biggest problem that the housing market has to deal with.

The “locked-in effect” describes a situation where homeowners with super-low mortgage rates try to hang on to that mortgage for as long as possible by not moving, thereby staying off the housing market entirely, both as seller and as buyer. It ultimately doesn’t change inventory because they’re neither buying nor not selling a house, thereby not taking one off the market and not putting one on the market. But it depresses home sales, which are down by 20% to 25% from 2018 and 2019.

The brokerage industry – which makes money coming and going when a homeowner changes homes – and the mortgage-lending industry are very upset about this locked-in effect on sales because it’s eating their lunch, and not just their lunch, but their jobs.

But turns out, these below-4% mortgages are not so locked in as homeowners find themselves confronted with a situation where they want to, or have to, pay off the low-interest-rate mortgage and take out a new mortgage at a much higher rate. And so homeowner by homeowner, the locked-in effect fades.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The post As Life Happens, “Locked-in” Homeowners Pay Off Below-4% Mortgages: Share Drops to 54%, Lowest since Q4 2020 appeared first on Energy News Beat.

“}]]